Table of Contents

Overview

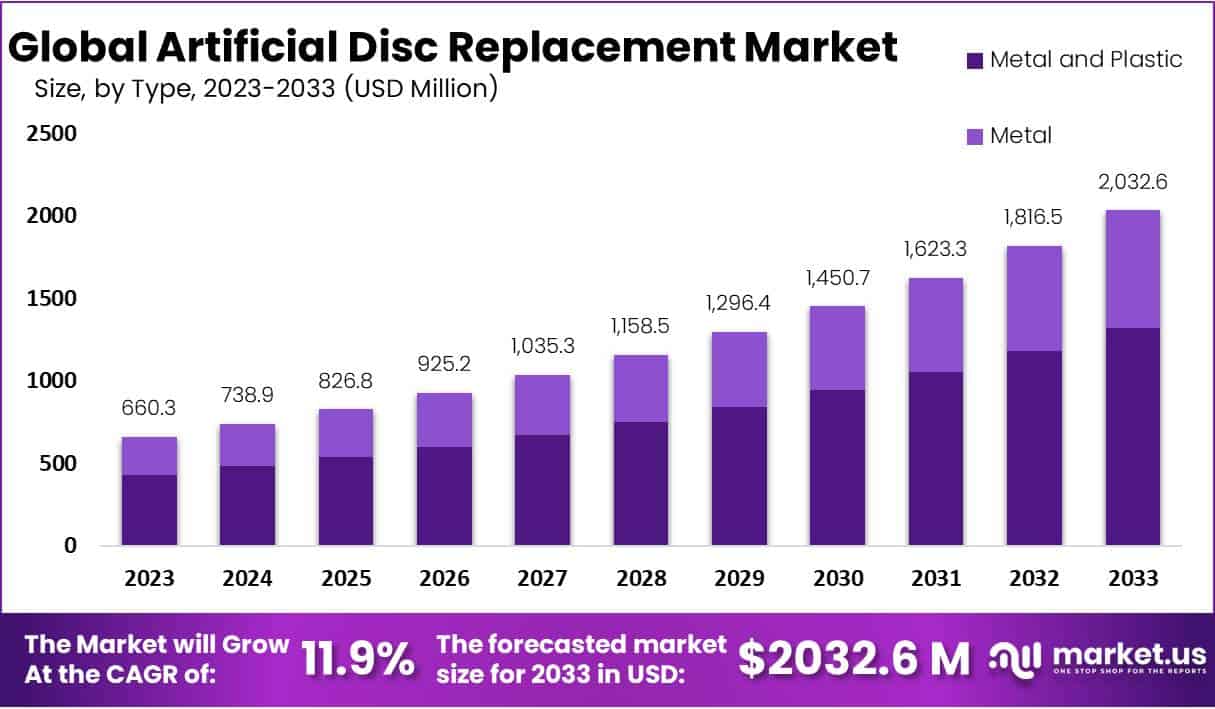

The Artificial Disc Replacement (ADR) Market is projected to grow strongly, reaching approximately USD 2,032.6 million by 2033, up from USD 660.3 million in 2023. This reflects a Compound Annual Growth Rate (CAGR) of 11.9% from 2024 to 2033. The market expansion is driven by the increasing prevalence of neck and back pain, aging demographics, supportive reimbursement policies, and a steady flow of regulatory approvals that strengthen product availability and innovation.

The prevalence of neck pain is expanding the candidate pool for cervical ADR. The Global Burden of Disease 2021 study projects 269 million neck-pain cases by 2050, up by one-third from 2020. This growing patient base underpins sustained procedure volumes. Additionally, the aging global population contributes significantly to demand growth. OECD data show the old-age to working-age ratio rising from 33 per 100 in 2024 to 55 per 100 by 2050, highlighting an increase in spine-related degenerative conditions.

Payment policies in large healthcare markets continue to favor ADR adoption. In the United States, the Centers for Medicare & Medicaid Services approved a 2.9% payment increase for Ambulatory Surgical Centers in 2025. This update supports outpatient spine procedures and encourages the transition of ADR cases from inpatient to ambulatory settings. Such policies enhance affordability, expand procedural access, and improve hospital efficiency by reducing inpatient loads.

Regulatory activities remain dynamic, reflecting a healthy innovation pipeline. The U.S. FDA approved several PMA supplements in 2024, including those for Simplify® and M6-C cervical disc systems. These approvals demonstrate ongoing product refinement, enhanced labeling, and stable market access for next-generation ADR technologies. The steady regulatory flow indicates confidence in product safety and sustained technological progress in motion-preserving implants.

Elective procedure recovery across OECD countries is further supporting market growth. Australia reported 778,500 elective admissions in 2023–24, a 5.8% year-over-year increase. Similarly, backlog pressures in the U.K. are prompting investments in faster elective capacity. Improved administrative datasets, such as AHRQ’s HCUP and England’s RTT reports, now enable better tracking of outcomes and utilization, driving data-led adoption of ADR. Combined with a persistent occupational musculoskeletal burden, these factors ensure sustained demand for cervical and lumbar disc replacement procedures.

Key Takeaways

- The Artificial Disc Replacement Market is projected to reach USD 2,032.6 million by 2033, growing at a strong CAGR of 11.9%.

- Metal and Plastic types dominated in 2023, capturing over 65% market share valued at USD 660.3 million, driven by superior durability and adaptability.

- Cervical Disc Replacement led with 53% share in 2023, primarily addressing degenerative issues affecting the neck and upper spinal regions.

- Continuous advancements in medical technology have enhanced artificial disc efficiency and reduced complications, driving overall market expansion.

- The global rise in the aging population significantly boosts demand for ADR, as degenerative disc diseases become more prevalent.

- High procedural costs remain a major limitation, restricting access to artificial disc replacement in cost-sensitive healthcare markets.

- Limited reimbursement frameworks continue to hinder market adoption, discouraging both patients and healthcare institutions in certain regions.

- Emerging economies present strong growth opportunities, supported by expanding healthcare infrastructure and increasing patient awareness.

- The trend toward personalized ADR solutions is gaining momentum, offering tailored treatments and improved patient outcomes.

- North America maintained market leadership in 2023 with over 49.2% share, supported by advanced healthcare systems and early adoption of technologies.

Regional Analysis

In 2023, North America held a leading position in the Artificial Disc Replacement (ADR) Market, accounting for over 49.2% of the total share. The region’s market value reached USD 324.8 million, highlighting its strong contribution to the global ADR landscape. Growth in this region can be attributed to a robust healthcare system, the growing prevalence of degenerative disc diseases, and advanced technology adoption. Favorable reimbursement policies and active healthcare innovation have further supported the increasing number of ADR procedures across the region.

The United States remains the major driver of this growth, supported by a large aging population and rising cases of chronic back pain. Strategic collaborations among healthcare institutions and technology providers have strengthened research and product innovation. Europe follows closely, led by Germany, the United Kingdom, and France, which benefit from modern healthcare systems and growing awareness of minimally invasive procedures. Meanwhile, Asia-Pacific is expected to experience rapid growth, driven by expanding healthcare infrastructure and increasing healthcare spending.

Segmentation Analysis

In 2023, the Metal and Plastic segment held a dominant position in the Artificial Disc Replacement market, accounting for over 65% of the total share. Its success was driven by the integration of metal’s strength with plastic’s flexibility, offering improved durability and adaptability. This combination ensured structural integrity and natural spinal movement. Patients benefited from enhanced mobility and reduced discomfort, increasing acceptance among healthcare professionals. Continuous innovations in material science and biocompatibility further strengthened its market leadership and long-term performance.

The Cervical Disc Replacement segment also led the Artificial Disc Replacement market in 2023, achieving a market share exceeding 53%. This dominance was attributed to the rising adoption of cervical procedures addressing neck-related spinal issues. The segment’s growth was further supported by technological advancements and improved surgical outcomes. Lumbar Disc Replacement followed closely, driven by the demand for lower back treatments. Increasing awareness, better procedural success rates, and continuous innovation are expected to sustain the momentum of both cervical and lumbar segments in the coming years.

Key Players Analysis

The Artificial Disc Replacement (ADR) market is shaped by a combination of technological innovation, clinical advancements, and strategic expertise. Leading manufacturers continue to redefine spinal care through advanced motion preservation systems and improved implant materials. Among these, Medtronic stands out for its strong research capabilities and extensive experience in spinal solutions. Its continuous product innovation and commitment to enhancing patient outcomes reinforce its leadership in the ADR landscape, while Orthofix Medical Inc. strengthens the field with its specialized orthopedic device portfolio and focus on procedural excellence.

A surge in technological integration and patient-centric designs has further intensified market competition. Companies such as Globus Medical and Aesculap Inc. have made significant contributions in this regard. Globus Medical emphasizes advanced spine technologies and minimally invasive procedures, ensuring better clinical outcomes and faster recovery. Aesculap Inc., known for its precision surgical instruments, enhances reliability and safety in spinal surgeries, addressing the growing demand for high-performance disc replacement systems with superior biomechanical compatibility.

Continuous innovation in motion preservation and implant design has accelerated the expansion of the ADR market. Organizations like NuVasive Inc. and AxioMed LLC are leading this transformation through next-generation disc technologies and a strong focus on natural mobility restoration. Their dedication to research-driven improvements and tailored product offerings aligns with the increasing clinical need for motion-preserving alternatives to spinal fusion, thereby strengthening their positions in the global ADR sector.

Strategic collaboration and product diversification remain central to long-term market sustainability. Industry contributors such as Zimmer Biomet, SpineArt SA, Synergy Spine Solutions Inc., and Centinel Spine are advancing innovation through R&D investments and global partnerships. Their collective efforts emphasize biocompatibility, patient safety, and long-term durability, creating a robust competitive environment. These ongoing initiatives ensure that the ADR market continues its trajectory of technological progress, enhanced surgical precision, and improved patient-centric care outcomes.

Market Key Players

- Medtronic

- Orthofix Medical Inc.

- Globus Medical

- Aesculap Inc.

- NuVasive Inc.

- AxioMed LLC

- Zimmer Biomet

- SpineArt SA

- Synergy Spine Solutions Inc.

- Centinel Spine

Conclusion

The Artificial Disc Replacement market is witnessing strong and steady growth, supported by the rising prevalence of spine-related disorders, technological advancements, and favorable healthcare policies. Increasing awareness of motion-preserving procedures and continuous innovation in implant materials are enhancing surgical outcomes and patient satisfaction. Market leaders are focusing on research-driven development and expanding access to advanced treatments worldwide. Although high procedural costs and limited reimbursement remain challenges, growing investments in healthcare infrastructure and the shift toward personalized treatment solutions are expected to create new opportunities. Overall, the market is positioned for long-term expansion, driven by innovation, accessibility, and improving clinical outcomes.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)