Table of Contents

Overview

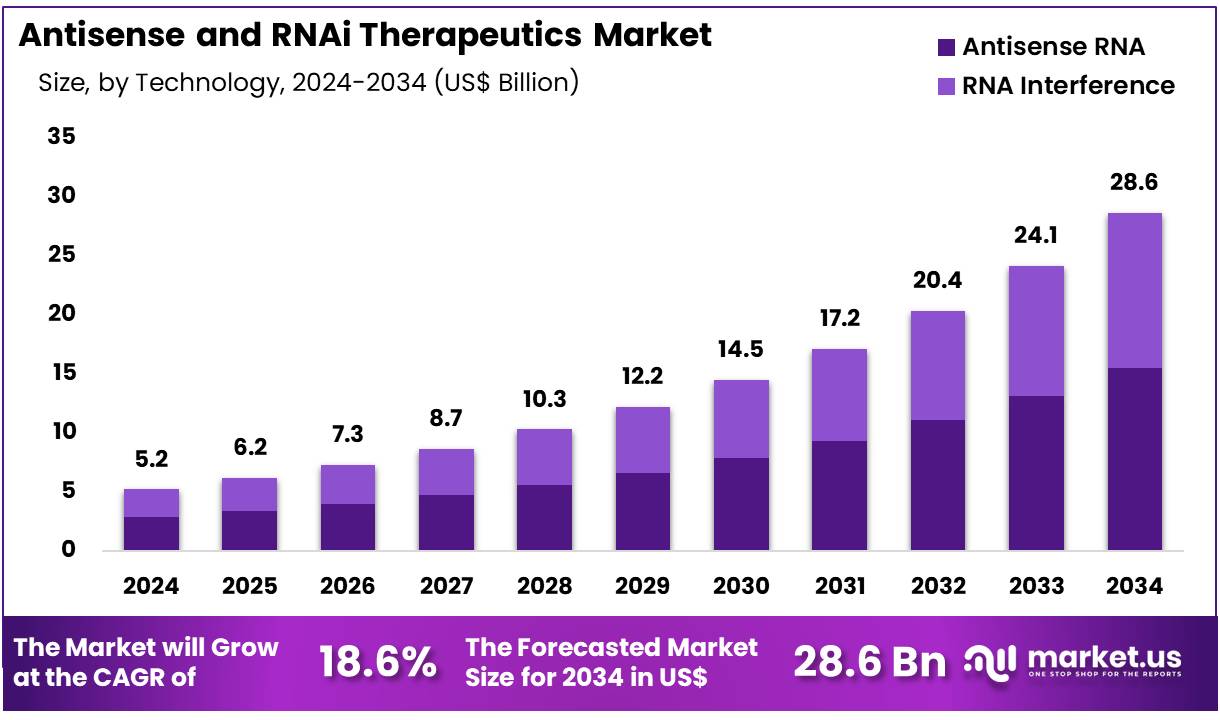

New York, NY – Nov 26, 2025 – Global Antisense and RNAi Therapeutics Market size is expected to be worth around US$ 28.6 Billion by 2034 from US$ 5.2 Billion in 2024, growing at a CAGR of 18.6% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 43.2% share with a revenue of US$ 1.0 Billion.

The global Antisense and RNAi Therapeutics market is experiencing steady expansion as innovative gene-silencing technologies continue to advance targeted treatment options for complex diseases. The growth of the market is being driven by rising investments in genetic research, increasing demand for precision medicine, and the expanding clinical pipeline focused on rare disorders, oncology, and metabolic conditions. Antisense oligonucleotides (ASOs) and RNA interference (RNAi) platforms have demonstrated improved therapeutic potential because disease-causing genes can be selectively inhibited at the molecular level.

A surge in regulatory approvals and accelerated designations has strengthened market confidence. The adoption of antisense therapies for neurological diseases has increased, while RNAi-based drugs have delivered strong clinical outcomes in hepatic and cardiometabolic indications. Strategic collaborations between pharmaceutical companies and biotech firms have supported the development of next-generation molecules with enhanced stability, specificity, and delivery efficiency. Continuous research activity in ligand-conjugated delivery systems is contributing to broader therapeutic applicability.

The market outlook remains positive, as rising prevalence of genetic and chronic diseases is creating sustained demand for targeted modalities. North America continues to lead due to advanced research infrastructure and favorable regulatory support, while Asia-Pacific is demonstrating rapid growth backed by expanding R&D capabilities and government investment. Overall, the sector is expected to evolve rapidly as improved RNA-targeting chemistries and delivery technologies move from research settings to commercial deployment.

Key Takeaways

- In 2024, the antisense and RNAi therapeutics market generated revenue of US$ 5.2 billion, and it is projected to grow at a CAGR of 18.6%, reaching US$ 28.6 billion by 2033.

- The technology segment is categorized into RNA interference and antisense RNA, with antisense RNA leading the market in 2024, accounting for 54.3% of the total share.

- Based on application, the market encompasses genetic disease, cancer, skin disorders, respiratory disorders, ocular disorders, neurodegenerative disorders, infectious disease, and cardiometabolic & renal disorders. Among these, neurodegenerative disorders represented the dominant application area with a 43.5% share in 2024.

- In terms of route of administration, the market is segmented into intravenous injections, subcutaneous injections, intrathecal injections, and others. The intrathecal injections category emerged as the leading segment, capturing 53.8% of the revenue share.

- Geographically, North America remained the leading regional market, holding a 43.2% share in 2024.

Regional Analysis

North America Leading the Antisense and RNAi Therapeutics Market

North America held the largest share of 43.2% in the Antisense and RNAi Therapeutics market, a position supported by substantial healthcare expenditure and strong research infrastructure. Healthcare spending in the United States reached US$ 4.5 trillion in 2022, as reported by the Centers for Medicare & Medicaid Services (CMS).

The region benefits from the presence of major biotechnology and pharmaceutical companies, consistent government and private funding, and a clear regulatory framework for novel therapeutics approved by the U.S. Food and Drug Administration. High awareness and adoption of advanced treatments for genetic disorders and cancer continue to support regional market expansion. Funding insights from the National Institutes of Health (NIH) in 2023 further highlight ongoing investment in nucleic acid–based research, strengthening the therapeutic pipeline in this space.

Asia Pacific Set to Register the Fastest CAGR

The Asia Pacific region is projected to record the highest CAGR during the forecast period, driven by rising healthcare expenditure and increasing access to advanced therapeutics. The World Bank reported steady growth in healthcare spending across East Asia and the Pacific in 2022, underscoring the region’s expanding medical infrastructure. Growing investments in biotechnology and pharmaceutical development in countries such as China and India are supporting market expansion.

The rising burden of cancer and genetic disorders in this populous region is creating strong demand for novel treatment modalities. Additionally, supportive regulatory reforms and improved domestic manufacturing capabilities are accelerating market growth. China’s National Medical Products Administration (NMPA) has been streamlining approval processes for innovative therapies, facilitating the development and commercialization of RNA-based treatments.

Emerging Trends

- Acceleration in FDA Approvals of Nucleic Acid-Based Therapies: The approval landscape for nucleic acid drugs has expanded rapidly. The U.S. FDA granted accelerated approval to tofersen (QALSODY) in April 2023 for SOD1-mutant ALS, representing the first antisense therapy for this condition. In the same year, vutrisiran received approval for hereditary transthyretin-mediated amyloidosis, administered quarterly through subcutaneous delivery. These advancements indicate increasing regulatory confidence in antisense and RNA interference (RNAi) modalities.

- Advances in Chemical Optimization and Precision Delivery: Substantial progress has been observed in chemical modification strategies that enhance stability, potency, and targeted delivery of oligonucleotide drugs. GalNAc-siRNA conjugation is now widely used to achieve efficient and selective hepatocyte targeting at lower doses. Modified chemistries such as locked nucleic acid (LNA) and constrained ethyl (cEt) designs provide increased nuclease resistance and high binding affinity, supporting the development of second-generation antisense oligonucleotides (ASOs) and siRNAs with improved therapeutic performance.

- Growth of Personalized and N-of-1 Antisense Therapeutics: The antisense platform has demonstrated viability for highly individualized treatment approaches. The development of milasen, a patient-specific ASO for Batten disease, provided a notable example of rapid design and emergency-use deployment within months. The feasibility of such customized therapeutics is expected to drive broader adoption of N-of-1 strategies for ultra-rare genetic disorders, supported by streamlined design and testing workflows.

- Expansion of the Late-Stage Clinical Pipeline: The clinical pipeline for oligonucleotide therapies has expanded to include a wider range of therapeutic areas. Multiple candidates have progressed to phase III development, such as tofersen for ALS and inclisiran for familial hypercholesterolemia. In a pivotal study with 482 participants, inclisiran achieved a 39.7% reduction in LDL-cholesterol at 16 months. This pipeline expansion reflects the increasing maturity and validation of oligonucleotide-based interventions across neurology, cardiometabolic diseases, and rare genetic conditions.

Use Cases

- Givosiran for Acute Hepatic Porphyria: Givosiran, a GalNAc-conjugated siRNA, reduces hepatic ALAS1 expression to prevent accumulation of toxic metabolites. In a 94-patient study, 74% of treated individuals experienced fewer porphyria attacks. Monthly dosing demonstrated sustained efficacy and acceptable tolerability, although routine monitoring of liver and kidney function is advised.

- Inotersen for Hereditary Transthyretin Amyloidosis (hATTR): Inotersen, incorporating 2′-O-MOE chemistry, targets TTR mRNA to decrease pathogenic protein levels. A 66-week, randomized phase III trial involving 112 treated and 60 placebo patients showed significant improvement in neuropathy impairment metrics. These findings confirmed the therapeutic value of inotersen for polyneuropathy associated with TTR mutations.

- Fitusiran for Hemophilia A and B: Fitusiran employs siRNA-mediated suppression of antithrombin to rebalance coagulation pathways. A phase II study with 25 participants demonstrated an 81% reduction in antithrombin mRNA, accompanied by a decline in annualized bleed rate from 12 to 1.7 events over 13 months. These results highlight strong efficacy in bleed prevention with monthly administration.

- Inclisiran for Heterozygous Familial Hypercholesterolemia: Inclisiran targets PCSK9 mRNA and is administered twice yearly. In a 482-subject phase III trial, the therapy achieved a 39.7% LDL-cholesterol reduction at 16 months, whereas the placebo group recorded an 8.2% increase. Approximately 65% of treated patients attained LDL-C concentrations below 100 mg/dL, underscoring consistent lipid-lowering durability and dosing convenience.

Frequently Asked Questions on Antisense and RNAi Therapeutics

- How do antisense therapies function?

Antisense therapies function by using synthetic oligonucleotides that bind to complementary RNA sequences. This binding blocks translation or triggers RNA degradation, reducing expression of targeted genes associated with various genetic, metabolic, and neurological disorders. - What is RNA interference (RNAi)?

RNA interference is a natural cellular process where small RNA molecules, such as siRNA or miRNA, inhibit gene expression. Therapeutic RNAi technologies harness this mechanism to silence specific genes involved in disease progression, enabling highly selective and durable treatment effects. - Which diseases are commonly treated using these therapies?

Antisense and RNAi therapies are used for genetic disorders, neurodegenerative diseases, cancer, metabolic disorders, and rare diseases. Their precision targeting makes them suitable for indications where conventional drugs demonstrate limited effectiveness or inadequate molecular specificity. - What advantages do these therapeutics offer?

These therapeutics offer targeted gene silencing, reduced off-target toxicity, and strong clinical potential for previously untreatable diseases. Their mechanism allows modulation of disease pathways at the RNA level, enabling long-lasting effects with improved therapeutic efficiency. - Which technology segment leads the market?

The antisense RNA segment currently leads the technology category due to established therapeutic platforms, successful product approvals, and widespread use in neurological disorders. Its strong clinical adoption supports its continued dominance over RNA interference therapies. - Which application segment holds the largest share?

Neurodegenerative disorders account for the largest share, supported by high disease burden and increasing reliance on gene-silencing strategies. Strong clinical evidence and multiple late-stage pipeline products contribute significantly to the segment’s leading market position. - Which region dominates the global market?

North America dominates owing to substantial healthcare expenditure, strong research capabilities, and supportive regulatory frameworks. The presence of major biotechnology companies and continued investment in nucleic acid therapeutics reinforce the region’s leadership.

Conclusion

The Antisense and RNAi Therapeutics market is positioned for sustained expansion as gene-silencing technologies gain broader clinical acceptance. Growth is being supported by rising investment in genetic research, an expanding late-stage pipeline, and increasing adoption across neurological, cardiometabolic, and rare disease applications.

Strong regulatory momentum and advances in delivery chemistries are enhancing therapeutic performance and commercial viability. North America maintains clear leadership, while Asia Pacific is emerging as the fastest-growing region due to rising healthcare spending and supportive policy reforms. Overall, the market is expected to advance rapidly as precision RNA-targeted therapies achieve broader global integration.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)