Table of Contents

Overview

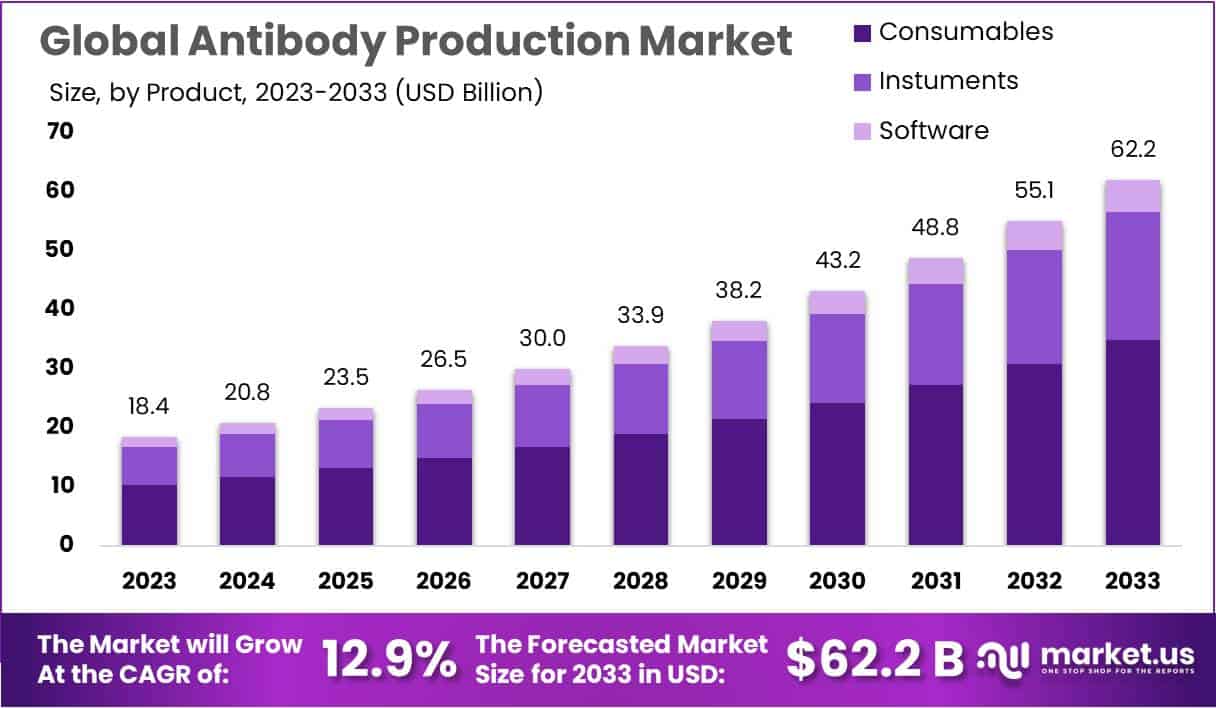

The Antibody Production Market is projected to grow significantly, reaching USD 62.2 billion by 2033, compared to USD 18.4 billion in 2023. This growth represents a CAGR of 12.9% between 2024 and 2033. Such expansion reflects rising demand for antibody-based therapies, supported by advanced bioprocessing technologies. Increasing investment in production capacity and innovation in upstream and downstream processes are strengthening the global supply chain for monoclonal antibodies and related biologics.

Demographic changes are playing a crucial role in this growth. The global rise in aging populations is creating consistent demand for biologic therapies used in cancer, autoimmune, and infectious diseases. United Nations data highlights that the share of individuals aged 65 and older continues to climb. This shift means higher treatment volumes, longer treatment durations, and a strong need for advanced antibody therapies. As a result, manufacturers are expanding capacity and upgrading technologies to meet growing therapeutic requirements.

Regulatory approvals are further supporting market momentum. The European Medicines Agency reported 77 positive recommendations for human medicines in 2023, many of which were biologics and vaccines. Similarly, the U.S. Food and Drug Administration continues to accelerate approvals for antibody-based agents, especially in oncology. These approvals confirm that scientific pipelines are rapidly translating into commercial products. With broader indications gaining clearance, demand for large-scale antibody production and related services continues to expand.

Public health policies are also reinforcing investments. The World Health Organization’s Immunization Agenda 2030 emphasizes the introduction of new vaccines and improved coverage. This framework pressures health systems and manufacturers to strengthen production infrastructure, cold-chain logistics, and quality systems. Such initiatives directly impact antibody platforms by driving improvements in bioprocessing efficiency and ensuring production networks remain resilient, particularly after the COVID-19 experience.

Regulatory Clarity and Strategic Growth Factors

Regulatory frameworks are creating confidence for large-scale investment in antibody production. WHO guidelines on monoclonal antibody quality control and EMA’s detailed product regulations provide clarity on process validation, potency, and stability. Such predictable regulatory science reduces technical risks and shortens development cycles. Manufacturers are now more willing to invest in upstream titer improvements, single-use technologies, and continuous processing, which directly enhance production efficiency and scalability.

Public funding is another catalyst shaping market expansion. The U.S. BARDA has allocated multi-year budgets to advance antibody therapeutics for priority pathogens. By derisking scale-up and supporting late-stage development, such funding guarantees anchor demand for antibody production. This procurement-linked financing strengthens visibility for contract development and manufacturing organizations while encouraging investment in flexible and repurposable production platforms.

The biosimilar pathway is expanding market accessibility. EMA approvals confirm biosimilars are interchangeable with reference products, ensuring equal efficacy and safety. This clarity supports wider adoption, drives volume throughput, and incentivizes investments in cost-efficient production processes. As biosimilars gain traction, manufacturers focus on high-yield cell lines and optimized purification technologies to balance affordability with quality, thereby broadening the market base.

Emerging health challenges further contribute to market demand. Antimicrobial resistance is driving renewed focus on antibody-based interventions. WHO has emphasized the need for novel anti-infective agents, aligning with investments in antibody discovery and flexible GMP facilities. At the same time, growing healthcare spending across OECD nations and sustained pharmaceutical R&D investments create a stable backdrop for market expansion. Faster approval pathways and active pharmacovigilance also shorten time-to-market, encouraging earlier commitments to large-scale production.

Key Takeaways

- The antibody production market is projected to achieve USD 62.2 billion by 2033, growing steadily at a robust CAGR of 12.9%.

- Consumables, led by media and chromatography resins, accounted for 56.1% of revenue in 2023, underlining their importance in efficient biomanufacturing processes.

- Downstream processing captured 67.8% market share in 2023, reflecting the industry’s strategic focus on advanced and efficient purification methodologies.

- Monoclonal antibodies dominated with a 63.9% market share in 2023, highlighting their strong role in targeted therapeutics and diagnostics applications.

- Pharmaceutical and biotechnology companies led end-use adoption, securing 56.7% share, which emphasized their critical role in advancing antibody production.

- Market growth is being propelled by rising therapeutic antibody demand, biotechnology advancements, and significant healthcare infrastructure investments worldwide.

- However, challenges such as high production costs, complex regulatory approvals, capacity constraints, and contamination risks continue to hinder expansion.

- Industry trends are marked by strategic collaborations, a growing emphasis on sustainability, and adoption of artificial intelligence for optimized antibody production.

- North America led with 39.5% share (USD 7.26 billion), driven by advanced facilities, while Asia-Pacific displayed the fastest growth momentum.

- The future of the market depends on continuous innovation, adaptation, and effective navigation of evolving regulatory frameworks by stakeholders.

Regional Analysis

In 2023, North America dominated the Antibody Production Market, accounting for more than 39.5% of the global share and generating USD 7.26 billion. The region emerged as the central hub for antibody production due to its advanced research facilities, strong infrastructure, and continuous investments in innovation. A significant concentration of leading industry players is found in North America, further reinforcing its leadership. This strong position reflects the region’s consistent emphasis on advanced technologies and its ability to attract large-scale investments.

Europe secured a stable position in the global antibody production market, maintaining a strong contribution to overall revenues. The region benefits from established biotechnology expertise, well-developed healthcare systems, and a high focus on research excellence. European countries actively participate in clinical trials and innovative antibody research, strengthening their role in the market. While North America leads, Europe provides a robust balance with its long-standing capabilities. This demonstrates the region’s strong commitment to scientific advancement and healthcare innovation.

Asia-Pacific is witnessing rapid expansion, driven by rising investments, growing healthcare demand, and significant progress in biotechnology. Countries such as China, India, and Japan are investing heavily in research infrastructure and technological capabilities. These developments position the region as an emerging growth engine for antibody production. Increased government support, expanding pharmaceutical industries, and the adoption of advanced production techniques further fuel market growth. As a result, Asia-Pacific is transforming into a key player and is expected to challenge established markets in the coming years.

Other regions, including the Middle East and Africa, are still developing their antibody production capabilities. Limited infrastructure, fewer research facilities, and resource constraints currently restrict growth. However, the region shows clear potential, with gradual progress and increasing interest from global players. Partnerships, strategic investments, and improved healthcare focus could unlock future opportunities. Although their market share remains comparatively small, ongoing developments indicate positive prospects. These regions may evolve as secondary growth markets, contributing to the global antibody production landscape in the long term.

Segmentation Analysis

In 2023, the consumables segment led the antibody production market with over 56.1% share. This dominance stemmed from the vital role of media, buffers, reagents, chromatography resins, and filtration products in the production process. These components are indispensable for ensuring the smooth functioning of bioreactors, chromatography, and filtration systems. As the backbone of the production chain, consumables provide stability, consistency, and efficiency, making them a key driver of industry growth and an essential area of focus for stakeholders and manufacturers.

The process analysis highlights downstream processing as the dominant phase, holding a share of over 67.8% in 2023. This phase, which involves purification and isolation, ensures antibodies meet required quality and purity standards. Growing demand for cost-effective and efficient purification has reinforced its prominence. While upstream processing remains essential for cell culture and fermentation, market preference indicates greater focus on refining and optimizing downstream activities. This underscores the industry’s emphasis on quality assurance and the delivery of highly purified therapeutic antibodies to meet stringent regulatory requirements.

In terms of type, monoclonal antibodies dominated the market with over 63.9% share in 2023. Their precision, uniformity, and targeted action have driven widespread adoption across therapeutic and diagnostic applications. Their ability to bind specific antigens has positioned them as indispensable tools in advanced medicine. Conversely, polyclonal antibodies maintained a supportive role, offering broad applicability in certain research and diagnostic settings. However, monoclonal antibodies continue to lead due to their therapeutic efficacy, reflecting the increasing specialization and focus on targeted therapies in global healthcare.

End-use analysis revealed that pharmaceutical and biotechnology companies commanded the largest share, accounting for over 56.7% in 2023. Their investment in research, development, and production infrastructure remains critical to market expansion. Research laboratories also contributed significantly, highlighting the importance of innovation and discovery in advancing antibody technologies. Meanwhile, contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs) played a supportive but growing role, offering specialized outsourced services. Together, these players form a collaborative ecosystem, ensuring a steady supply of high-quality antibodies to meet global demand.

Key Players Analysis

Illumina is a leading player in the Antibody Production Market. The company’s genomic sequencing technologies provide unmatched precision in exploring antibody characteristics. These innovative platforms help researchers gain detailed insights into antibody structures and functions. Illumina’s strong commitment to advancing genomic research plays a crucial role in transforming antibody production methods. By offering advanced sequencing tools, the company supports the development of efficient solutions. This contribution accelerates antibody-related research and drives improvements in overall production workflows, making Illumina a critical market contributor.

Thermo Fisher Scientific is another major force in the Antibody Production Market. The company offers a wide portfolio of life sciences solutions. Its expertise covers all stages of antibody research, from development to large-scale production. Researchers benefit from robust, reliable tools that ensure efficiency and quality in manufacturing. Thermo Fisher’s comprehensive offerings support the acceleration of innovations in antibody production. With a global footprint and proven experience, the company strengthens advancements across antibody research. Its presence continues to provide stability and leadership within the competitive antibody production landscape.

Pacific Biosciences and BGI also bring significant value to the Antibody Production Market. Pacific Biosciences focuses on long-read sequencing, enabling deeper analysis of antibody structures. This approach supports enhanced production processes and the creation of superior antibodies. BGI contributes through its expertise in genomics, optimizing antibody development workflows worldwide. Its collaborative strategies and global presence broaden market growth. Alongside these leaders, smaller specialized players add diversity. Their niche technologies drive innovation, address specific research needs, and strengthen the overall competitiveness of the antibody production ecosystem.

Challenges

1) Complex Upstream Biology

Achieving high and stable titers remains a challenge in antibody production. Even advanced CHO processes do not always ensure consistent outcomes. Titers and glycosylation patterns can shift depending on media, feed strategies, and pH control. These changes affect both yield and product quality. For example, a fed-batch process at pH 7.2 achieved about 6.1 g/L while lowering high-mannose glycans. This shows that improvements are possible, but results are highly sensitive to conditions. Continuous monitoring and careful optimization are necessary to stabilize upstream performance and maintain product quality.

2) Downstream Bottlenecks and Cost

Downstream processing is still a major bottleneck in antibody manufacturing. Purification steps, such as Protein A chromatography, are expensive and capacity-limited. When upstream titers are intensified, downstream costs increase due to higher buffer needs and longer processing times. Unless the entire process is redesigned, efficiency gains upstream simply shift the problem downstream. Hybrid and continuous purification methods are being developed to address these issues. Adoption is ongoing, but large-scale use remains limited. The cost and complexity of downstream operations continue to drive research into alternative, scalable, and more economical solutions.

3) Regulatory and Comparability Demands

Regulatory compliance is a critical challenge for antibody and biosimilar production. Manufacturers must prove consistent quality, safety, and efficacy for every product. Any change in the production process requires comparability studies to confirm equivalence. These exercises can be resource-intensive and time-consuming. In 2024, the FDA proposed removing routine switching studies for biosimilar interchangeability. This change may simplify some development paths, but expectations for compliance remain strict. Companies must continue to invest in robust analytics, quality systems, and documentation to satisfy evolving regulatory frameworks while minimizing delays and costs in product approval.

4) Supply Chain and Single-Use Sustainability

Single-use technology (SUT) has become widely used in antibody production. It reduces cleaning requirements and lowers contamination risks. However, it creates trade-offs. The large amount of plastic waste raises concerns about environmental impact. Life-cycle assessments suggest SUT can be more sustainable than stainless steel when water and energy use are included. Still, end-of-life waste management remains a challenge. The industry is exploring recycling solutions and better infrastructure to handle plastic streams. Balancing operational efficiency with sustainability goals is becoming a key focus in the supply chain and facility design for antibody manufacturing.

5) Talent, Technology Integration, and Validation

The shift toward intensified or continuous operations requires new expertise. Skilled staff are needed to manage advanced sensors, digital tools, and process control strategies. Training and talent development are now essential for successful implementation. Technology integration also requires significant capital investment and careful validation. End-to-end transformation of facilities and workflows is complex and time-intensive. Robust analytics and automation must be developed and validated to ensure process reliability. Companies face challenges in balancing innovation with regulatory expectations while securing the workforce and infrastructure needed for a future-ready production system.

Opportunities

1) Demand Growth from Novel Formats and Indications

The biologics pipeline is strong, with dozens of approvals each year from the FDA. These include antibodies and advanced modalities that increase demand for manufacturing capacity and CDMO services. Biosimilars are also gaining ground. After a slowdown in 2023, U.S. approvals rose sharply in 2024 and continue in 2025. This growth is widening patient access and driving the need for efficient large-scale production. As the market expands, CDMOs will see rising opportunities in meeting demand for both innovative biologics and biosimilars, positioning themselves as essential partners for speed, quality, and cost efficiency.

2) Process Intensification and Continuous Manufacturing

Process intensification and continuous manufacturing are changing antibody production. Continuous or hybrid systems cut cost-of-goods and raise throughput. They also improve process robustness and sustainability. Economic studies confirm that well-executed systems lower production footprints. Hybrid models are now emerging, enabling higher productivity without compromising glycosylation stability. These solutions provide practical transition paths for manufacturers that cannot shift to full continuous operations immediately. Adoption of such systems will drive cost efficiency and reduce environmental impact, making them increasingly attractive in competitive biologics markets. They also create opportunities for CDMOs that specialize in process innovation and sustainable manufacturing platforms.

3) Smarter Upstream: Media, Feeds, and Cell-Line Engineering

Upstream innovation is boosting productivity in antibody manufacturing. Targeted design of media and feeds, combined with pH and process control, increases titers while safeguarding quality. Cell-line engineering is also advancing. Tools ranging from vector optimization to glyco-engineering are enabling better performance of recombinant mAb platforms. Contemporary CHO systems now deliver high product concentrations, supported by refined controls. These advancements create a strong foundation for further gains in yield and consistency. Manufacturers that adopt smarter upstream strategies can achieve competitive cost and quality advantages. As demand grows, these methods will be essential to scaling supply efficiently and sustainably.

4) Single-Use and Modular Facilities

Single-use technologies (SUT) are transforming facility design in biologics. They allow faster changeovers, flexible production scales, and reduced utilities. Life cycle analyses show that SUT systems often perform better than stainless steel, especially in regions with high water and energy costs. Recycling and circular solutions are also progressing, strengthening sustainability outcomes. Modular facilities equipped with single-use systems provide agility to adapt quickly to demand shifts or new molecule types. As biologics pipelines diversify, such setups will gain favor among CDMOs and manufacturers. They represent a practical balance of efficiency, flexibility, and environmental responsibility in antibody production.

5) Regulatory Evolution That May Reduce Friction

Regulatory frameworks are evolving to ease development pathways. A recent FDA proposal removes the need for routine switching studies to gain interchangeability for biosimilars. This adjustment could shorten approval timelines and reduce costs for developers. With fewer hurdles, more biosimilar entrants are expected. Increased competition may drive down prices and broaden patient access. For manufacturers, this creates a strong incentive to enhance efficiency and cost control. CDMOs and innovators that align with evolving regulatory expectations will benefit from faster time-to-market. These changes highlight the importance of agility in navigating shifting regulatory landscapes in antibody production.

6) Expanding Indications and Formats (Bispecifics, ADCs)

Antibody formats are becoming more complex, creating new opportunities for specialized manufacturing. Bispecifics and antibody-drug conjugates (ADCs) are now gaining regulatory approvals at a growing pace. These advanced molecules require tailored upstream and downstream processes to manage potency, stability, and safety. The demand for expertise in handling high-potency or multi-specific formats is expanding. This trend is opening market niches for innovators and CDMOs with advanced technical capabilities. As pipelines diversify into oncology, autoimmune, and rare diseases, the need for specialized solutions will grow. This shift strengthens opportunities for differentiation and long-term partnerships in the antibody market.

Conclusion

The antibody production market is set for strong and steady growth, supported by rising demand for targeted therapies and continuous innovation in bioprocessing. Increasing investments, supportive regulatory frameworks, and the adoption of advanced technologies are shaping a favorable environment for expansion. While challenges such as high costs, complex production steps, and sustainability concerns remain, opportunities are emerging through process intensification, biosimilars, and advanced antibody formats. Growing healthcare needs and demographic shifts are also boosting demand worldwide. With North America leading today and Asia-Pacific showing the fastest momentum, the market’s future depends on innovation, collaboration, and effective responses to evolving health and regulatory priorities.

View More

Antibody Drug Conjugates Market || TCR-Based Antibody Market || Custom Antibody Services Market || Antibody Discovery Market || Antibody Therapy Market || Antibody Therapeutics Market || Complement C4 Antibody Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)