Table of Contents

Overview

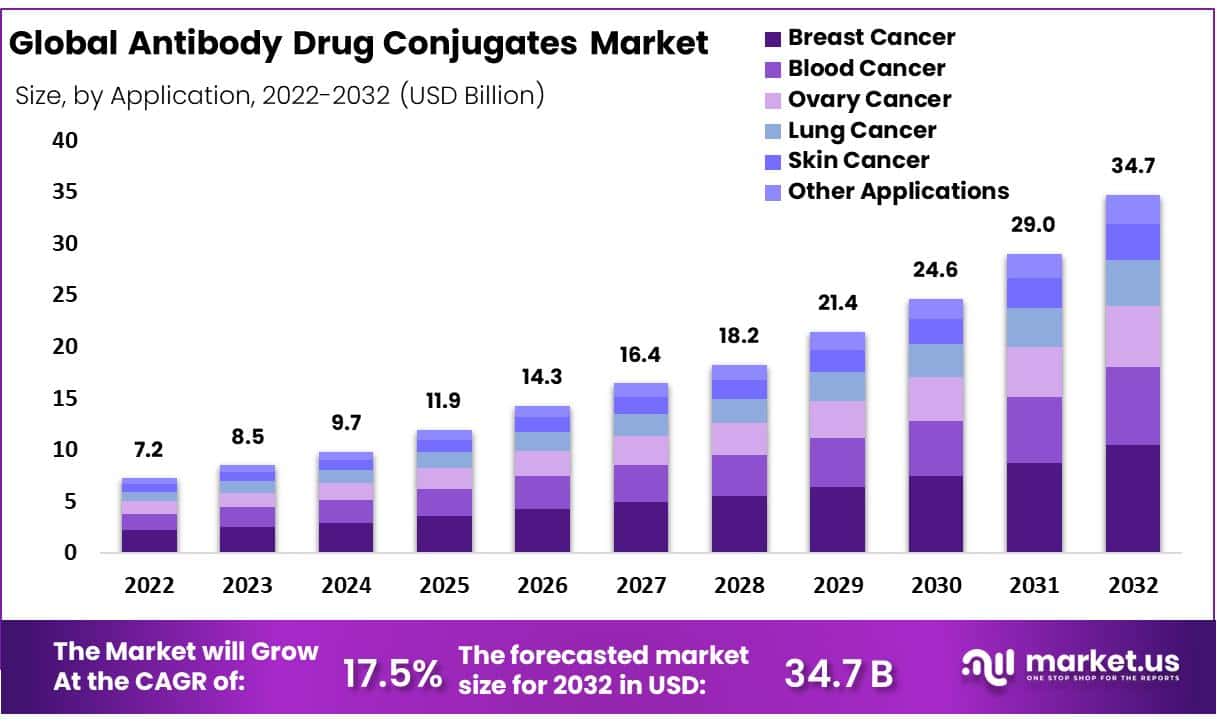

New York, NY – Aug 22, 2025 – In 2024, the global Antibody Drug Conjugates Market accounted for USD 9.7 billion and is expected to grow to around USD 34.7 billion in 2032. Between 2025 and 2032, this market is estimated to register the highest CAGR of 17.5%.

Antibody Drug Conjugates (ADCs) represent one of the most advanced innovations in oncology therapeutics, combining the precision of targeted antibodies with the potency of cytotoxic drugs. The formation of an ADC involves three key components: a monoclonal antibody, a cytotoxic payload, and a chemical linker.

The monoclonal antibody is designed to recognize and bind specifically to antigens expressed on the surface of cancer cells. Once bound, it serves as a delivery vehicle, ensuring that the therapeutic effect is directed only toward malignant cells, thereby reducing damage to healthy tissues. The cytotoxic payload, often too toxic to be administered alone, is a highly potent drug capable of inducing cell death. Its targeted delivery enhances efficacy while minimizing systemic toxicity.

The linker plays a crucial role in maintaining the stability of the ADC during circulation in the bloodstream. It ensures that the drug is released only after the antibody binds to the target cell and is internalized. This controlled release mechanism is critical to the success of ADC therapies.

The strategic integration of these three components has enabled ADCs to achieve significant clinical milestones, with several therapies already approved and many more in development. ADCs are reshaping the landscape of cancer treatment, offering hope for improved patient outcomes and a new era of precision medicine.

Key Takeaways

- Market Growth: The global Antibody Drug Conjugates (ADCs) market was valued at USD 9.7 billion in 2024 and is projected to reach USD 34.7 billion by 2032, registering a CAGR of 17.5% during 2025 –2032.

- Rising Cancer Incidences: The increasing prevalence of cancer worldwide is a major growth driver. ADCs offer targeted delivery of cytotoxic agents directly to cancer cells, minimizing damage to healthy tissues and improving treatment precision.

- Application Analysis: Breast cancer treatment currently accounts for the largest share of the ADC market, supported by the growing number of regulatory approvals. Blood cancers are also anticipated to capture a significant share in the coming years.

- Technology Analysis: Cleavable linkers dominate the market due to their stability in the bloodstream and controlled release of cytotoxins. This segment is expected to maintain its strong growth trajectory.

- Product Analysis: Non-cleavable linkers, exemplified by Kadcyla in breast cancer therapy, are gaining traction. Their high stability makes them effective even in antigen-negative cells.

- End-User Analysis: Hospitals and specialty cancer centers remain the leading end-users of ADCs, as they provide the infrastructure to manage side effects and administer treatments effectively.

- Market Drivers: Key drivers include technological advancements, rising cancer prevalence, supportive government initiatives, and the expansion of healthcare systems globally.

- Market Restraints: High production costs, side effects, and challenges related to raw materials and skilled labor continue to limit market expansion.

- Opportunities: Government initiatives in cancer prevention, alongside public-private partnerships, are expected to create new growth opportunities.

- Emerging Trends: The adoption of ADCs is increasing due to their targeted approach. Multiple FDA approvals have boosted market confidence, and post-COVID recovery is expected to further accelerate demand.

- Regional Insights: North America leads the global ADC market with a 40% share, driven by high healthcare expenditure. Europe follows, supported by a growing cancer patient base.

- Key Players: Leading companies are focusing on product innovation, regulatory approvals, and strategic mergers & acquisitions to strengthen their market presence.

Company Analysis

Takeda Pharmaceutical Company Limited: Takeda has reinforced its ADC portfolio through notable regulatory and strategic advancements. The European Commission approved ADCETRIS (brentuximab vedotin) in combination with chemotherapy for adult patients with stage IIb Hodgkin lymphoma, marking an expanded indication and strengthening its clinical presence. Furthermore, Takeda entered into a licensing agreement with ImmunoGen, securing rights to its ADC technology. This agreement involves an upfront payment along with potential milestone payments and royalties, aimed at bolstering Takeda’s ADC research and development capabilities. These initiatives underscore Takeda’s long-term commitment to advancing targeted oncology therapies and maintaining competitiveness in the rapidly growing ADC landscape.

Pfizer, Inc.: Pfizer has significantly expanded its ADC portfolio through regulatory approvals, clinical progress, and collaborations. The U.S. FDA granted full approval for Tivdak (tisotumab vedotin) for recurrent or metastatic cervical cancer, strengthening its oncology offerings. Additionally, Pfizer broadened its AI-driven ADC payload design partnership with PostEra, raising the collaboration’s total value to US$ 610 million. The company also presented Phase 1 data for two novel ADCs sigvotatug vedotin and a PD-L1-directed ADC in combination with pembrolizumab for thoracic cancers. Moreover, interim trial results for Padcev plus Keytruda demonstrated improved survival in muscle-invasive bladder cancer, with regulatory discussions anticipated. These advances affirm Pfizer’s leadership in ADC innovation.

AstraZeneca: AstraZeneca, in collaboration with Daiichi Sankyo, continues to dominate the ADC market with Enhertu, its HER2-targeting therapy. Enhertu generated approximately US$ 3.75 billion in global sales during 2024, highlighting exceptional commercial momentum and sustained demand. The therapy has established itself as a market leader within HER2-positive cancers, benefiting from robust adoption across key regions. AstraZeneca’s strategic collaboration with Daiichi Sankyo continues to drive innovation and commercialization, ensuring strong positioning in the ADC space. This performance not only reinforces AstraZeneca’s reputation as a leader in targeted oncology but also underlines its ability to capture significant market value in the ADC segment.

Gilead Sciences, Inc.: Gilead Sciences reported solid growth in its ADC portfolio, led by the Trop-2-directed therapy Trodelvy. In 2024, Trodelvy achieved approximately US$ 1.315 billion in global sales, reflecting strong market uptake and reinforcing its therapeutic relevance. This commercial success highlights Trodelvy’s increasing adoption for breast cancer and other approved indications. Gilead’s performance underscores its strengthening foothold in the ADC landscape, driven by a combination of clinical efficacy and expanding patient demand. With continued focus on oncology innovation, Gilead is positioned to leverage Trodelvy’s momentum while exploring future pipeline opportunities to enhance its share of the competitive ADC market.

Astellas Pharma, Inc.: Astellas Pharma has established a strong presence in the ADC market through its co-development of Padcev with Pfizer. In 2024, global sales of Padcev reached US$ 1.588 billion, reflecting substantial year-on-year growth. The drug has demonstrated robust clinical efficacy, particularly in urothelial cancer, cementing its importance as a breakthrough therapy. This performance highlights Astellas’ ability to capture significant value from strategic collaborations in oncology. By leveraging joint expertise, the company continues to reinforce its ADC portfolio and strengthen its competitive position in the global oncology therapeutics market, aligning with its broader growth strategy in innovative cancer treatments.

Seagen, Inc.: Seagen, now fully acquired by Pfizer, continues to benefit from the commercial success of its flagship ADC, ADCETRIS (brentuximab vedotin). In 2024, combined global sales of ADCETRIS reached US$ 1.911 billion, underscoring its sustained importance in the lymphoma treatment landscape. Despite no new product launches or acquisitions reported during the period, Seagen remains a critical asset within Pfizer’s oncology portfolio. Its expertise in ADC development, combined with Pfizer’s global reach, positions the company to further expand its influence in targeted therapies. ADCETRIS remains a cornerstone product, driving revenue and strengthening Seagen’s legacy within the ADC segment.

Daiichi Sankyo Company, Limited: Daiichi Sankyo has maintained a leadership role in the ADC space, driven by its partnership with AstraZeneca on Enhertu. In 2024, Enhertu achieved approximately US$ 3.754 billion in sales, affirming its dominance as a HER2-directed therapy. Beyond this, Daiichi Sankyo expanded its ADC portfolio with the co-marketing of Datroway (datopotamab deruxtecan), recently approved in China, reinforcing the company’s pipeline diversification and global expansion strategy. These achievements illustrate Daiichi Sankyo’s commitment to advancing next-generation ADCs and underline its ability to capture significant commercial success while maintaining a leadership position in the global oncology therapeutics market.

GlaxoSmithKline plc (GSK): GlaxoSmithKline’s ADC portfolio has demonstrated limited traction, with Blenrep (belantamab mafodotin) reporting modest sales of approximately £2 million in 2024. The therapy’s restricted uptake highlights ongoing challenges in commercialization and competitive positioning within the ADC market. No new ADC launches or acquisitions were reported during the review period, reflecting a cautious approach in this therapeutic class. Despite these challenges, GSK maintains a presence in oncology through its existing pipeline, though ADC-focused growth remains constrained. The company may require renewed strategic initiatives or collaborations to enhance its competitive standing in the ADC segment.

ADC Therapeutics SA: ADC Therapeutics continues to experience limited visibility in the global ADC market. Its lead product, Zynlonta (loncastuximab tesirine), reported modest past sales, such as US$ 69.1 million, with no significant updates for 2024. While Zynlonta remains an important therapy in the treatment of relapsed or refractory large B-cell lymphoma, its growth potential appears constrained compared to leading competitors. The company faces challenges in scaling commercialization and expanding pipeline traction. To improve market standing, ADC Therapeutics will likely need to pursue strategic partnerships, innovation in its pipeline, or broader geographic expansion initiatives.

ImmunoGen Inc.: ImmunoGen marked a pivotal milestone in November 2023 when AbbVie completed its acquisition of the company for US$ 10.1 billion. This consolidation integrated ImmunoGen’s ADC technology and pipeline assets into AbbVie’s expansive oncology portfolio, representing one of the largest deals in the ADC sector. The acquisition is expected to significantly strengthen AbbVie’s presence in targeted cancer therapies, leveraging ImmunoGen’s expertise in ADC innovation. For ImmunoGen, the transaction underscores its value as a key developer in the ADC landscape, while for AbbVie, it provides a strategic advantage to compete more aggressively in oncology.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)