Table of Contents

Overview

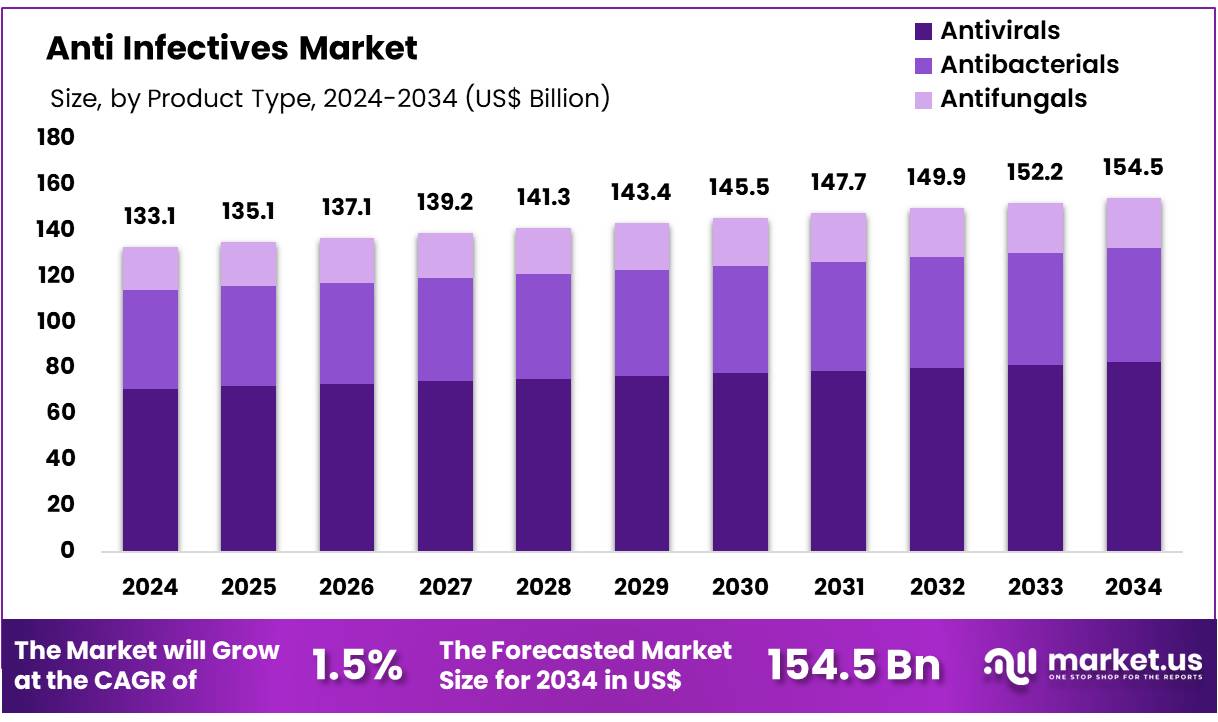

New York, NY – Nov 26, 2025 – Global Anti Infectives Market size is expected to be worth around US$ 154.5 billion by 2034 from US$ 133.1 billion in 2024, growing at a CAGR of 1.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.1% share with a revenue of US$ 52.0 Billion.

The global Anti-Infectives market has been witnessing steady expansion as the burden of infectious diseases continues to escalate worldwide. Rising incidences of bacterial, viral, fungal, and parasitic infections have accelerated the demand for advanced therapeutic agents. The growth of the market can be attributed to the increasing prevalence of antimicrobial-resistant pathogens, which has created the need for innovative treatments and next-generation drug formulations.

Continuous product development, expanding vaccination programs, and supportive government initiatives have contributed to sustained market growth. Accelerated approvals for novel antibiotics and antiviral drugs have strengthened the competitive landscape, while public–private partnerships have enhanced research productivity in critical therapeutic categories such as multidrug-resistant infections and emerging viral threats.

The Anti-Infectives market has been supported by significant investments in R&D activities, enabling the development of high-efficacy drug classes and combination therapies. Technological advancements in molecular diagnostics have improved early disease detection, thereby increasing treatment adoption. The availability of generic formulations has further broadened accessibility in low- and middle-income regions.

North America continues to hold a substantial share due to strong healthcare infrastructure and robust clinical pipelines. However, Asia-Pacific is projected to register notable growth driven by large patient populations and increasing healthcare expenditure.

The Anti-Infectives market is expected to maintain a positive growth trajectory as global health systems prioritize infection management and preparedness. Rising awareness, strategic collaborations, and expanding treatment portfolios are anticipated to support long-term market stability

Key Takeaways

- In 2024, the anti-infectives market generated revenue of US$ 133.1 billion and recorded a CAGR of 1.5%, with the market value projected to reach US$ 154.5 billion by 2033.

- The product type segment comprises antibacterials, antivirals, and antifungals, with antivirals accounting for the leading share of 53.5% in 2024.

- Based on route of administration, the market includes topical, parenteral, oral, and others, with the oral route holding a substantial 58.7% share.

- Within the distribution channel segment hospital pharmacies, retail pharmacies, and others—the hospital pharmacies category dominated, representing 61.2% of total revenue.

- North America emerged as the leading regional market, capturing 39.1% of the global share in 2024.

Regional Analysis

North America Leading the Anti-Infectives Market

North America accounted for the largest revenue share of 39.1%, driven by heightened concerns regarding antibiotic resistance and the consistent need for effective infectious disease management. According to the Centers for Disease Control and Prevention (CDC), six bacterial antimicrobial-resistant hospital-onset infections continued to remain above pre-pandemic levels in 2022 after peaking in 2021, emphasizing the sustained requirement for advanced anti-infective solutions.

Regulatory progress also supported market expansion. The US Food and Drug Administration (FDA) approved 50 new molecular entities in 2024, including three antibiotics Exblifep (cefepime and enmetazobactam), Zevtera (ceftobiprole medocaril sodium), and Orlynvah (sulopenem etzadroxil and probenecid). In addition, GSK secured FDA approval in March 2025 for Blujepa (gepotidacin), an oral treatment for uncomplicated urinary tract infections. These developments reflect the steady introduction of new therapies aimed at addressing drug-resistant pathogens.

Asia Pacific Expected to Register the Highest CAGR

Asia Pacific is projected to record the fastest growth rate during the forecast period due to the high prevalence of infectious diseases and the rising incidence of antimicrobial resistance. As highlighted by the World Health Organization (WHO) in 2024, antimicrobial resistance is responsible for more than 700,000 deaths globally each year, with a major share reported in Asia.

Evidence from the China Gonococcal Resistance Surveillance Program (China-GRSP) revealed increasing resistance to ceftriaxone an essential therapy for gonorrhea from 2017 to 2022. In response, China’s National Health Commission released guidelines in 2021 aimed at promoting the rational use of antibiotics and enhancing surveillance systems.

The persistent burden of diseases such as tuberculosis and dengue, combined with national efforts to curb resistance, is expected to contribute significantly to the growing demand for anti-infective treatments across the Asia Pacific region.

Emerging Trends

- Escalating Antimicrobial Resistance: Antimicrobial resistance continues to represent a significant global health burden. More than 2.8 million resistant infections are reported annually in the United States, leading to over 35,000 deaths. At the global level, bacterial resistance was associated with an estimated 1.27 million deaths in 2019 and contributed to approximately 4.95 million deaths when considering related factors.

- Expansion of the Antibiotic Development Pipeline: A gradual expansion of the antibacterial development pipeline has been observed, with the number of clinical candidates rising from 80 in 2021 to 97 in 2023. This growth reflects increased investment activity; however, the current pace remains insufficient to counter the accelerating resistance landscape.

- Refined Pathogen Prioritization: The 2024 update of the WHO Bacterial Priority Pathogens List identifies 24 antibiotic-resistant pathogens across 15 families. The revision places strong emphasis on critical priority Gram-negative organisms and drug-resistant Mycobacterium tuberculosis, providing a clearer framework to direct global research and development initiatives.

- Increased Modeling of Healthcare-Associated Infections: Enhanced modeling efforts by the CDC, including the MInD network, are being utilized to simulate transmission pathways of healthcare-associated infections, particularly those involving resistant strains. These analytical models indicate that HAIs have increased markedly in recent decades and offer evidence-based insights for improving prevention strategies.

Frequently Asked Questions on Anti Infectives

- How do anti-infectives work?

Anti-infectives operate through mechanisms such as disrupting cell wall synthesis, inhibiting protein production, or blocking replication pathways. These mechanisms weaken pathogens, enabling the body’s immune system to eradicate infections more effectively and limit disease progression. - What are the main types of anti-infectives?

The category includes antibiotics, antivirals, antifungals, and antiparasitic drugs. Each type targets specific pathogens and is developed to ensure precise therapeutic action, minimizing resistance risk and ensuring broader disease coverage across diverse infectious conditions. - Why are anti-infectives important in healthcare?

Anti-infectives play a critical role in reducing mortality, preventing outbreaks, and supporting routine medical procedures. Their use enables safe surgeries, protects vulnerable populations, and ensures that infectious diseases are controlled, thereby improving global public health outcomes. - What factors contribute to anti-infective resistance?

Resistance emerges due to misuse, overuse, incomplete treatment courses, and genetic mutations within microorganisms. These conditions create selective pressure that enables resistant strains to survive and spread, reducing drug effectiveness and complicating infection management. - What is driving growth in the anti-infectives market?

Market expansion is driven by rising infectious disease incidence, antimicrobial resistance challenges, increased R&D investments, and the introduction of novel therapies. These factors collectively stimulate demand for advanced treatment options and strengthen the global pharmaceutical landscape. - Which regions dominate the anti-infectives market?

North America leads due to strong healthcare infrastructure, high awareness, and significant pharmaceutical R&D activity. Europe follows closely, while Asia-Pacific shows rapid growth driven by population density, rising healthcare expenditure, and expanding access to medical treatment. - What future trends are shaping the market?

Future trends include the development of targeted therapies, growth of combination treatments, expansion of rapid diagnostics, and increased government support. These innovations are expected to enhance treatment outcomes and strengthen the overall anti-infectives market outlook.

Conclusion

The global anti-infectives market is projected to maintain steady growth as infectious disease prevalence and antimicrobial resistance continue to rise worldwide. Advancements in diagnostics, strong R&D investments, expanding treatment portfolios, and supportive regulatory actions have reinforced market expansion. High-efficacy therapies, broader vaccination coverage, and increased generic availability have strengthened accessibility, especially in emerging economies.

North America remains the dominant region due to robust healthcare infrastructure, while Asia-Pacific is expected to witness the fastest growth driven by rising disease burden and healthcare spending. Overall, sustained innovation, strategic collaborations, and global preparedness efforts are anticipated to secure long-term market stability.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)