Table of Contents

Introduction

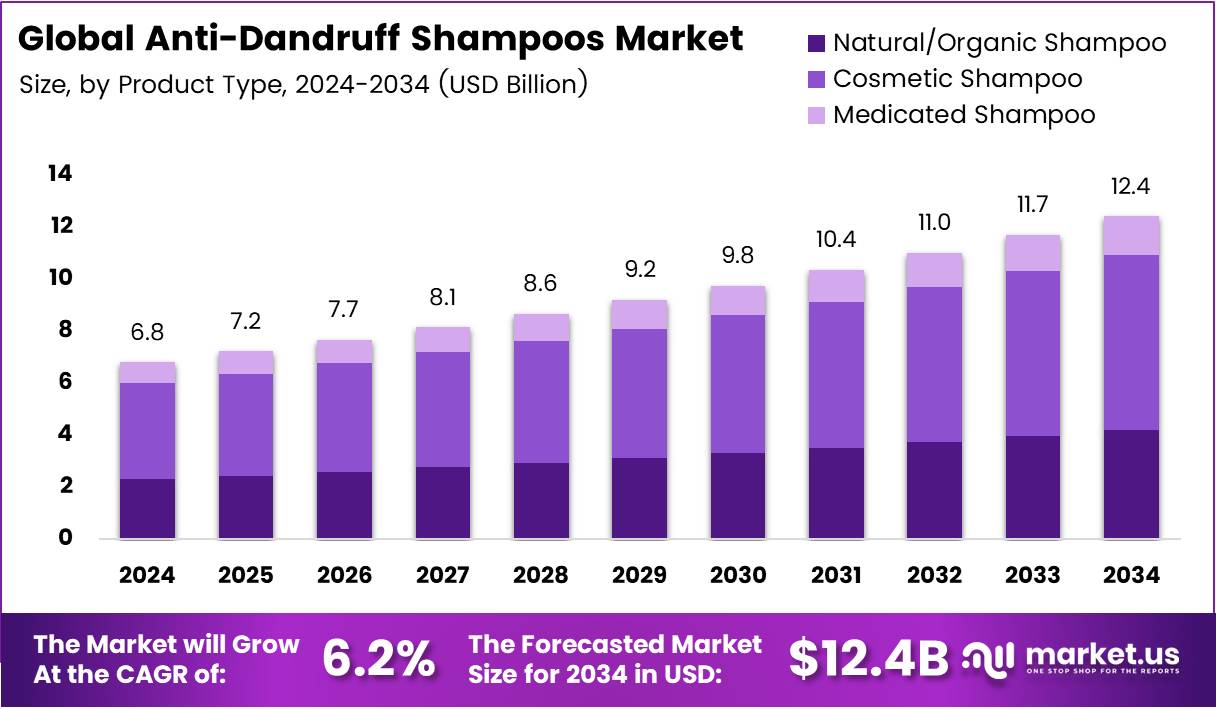

The global Anti-Dandruff Shampoos Market is entering a decisive growth phase, projected to reach USD 12.4 Billion by 2034, up from USD 6.8 Billion in 2024, at a CAGR of 6.2% from 2025–2034. Rising scalp-health awareness, cleaner-label innovation, and omnichannel access are accelerating adoption across demographics and geographies.

Moreover, consumers increasingly demand dermatologist-validated efficacy paired with pleasant sensorials and sustainability. As brands reformulate with microbiome-friendly and sulfate-free systems, they unlock premiumization while preserving clinical performance. Meanwhile, AI-enabled diagnostics and subscription models deepen engagement, recurring revenue, and regimen adherence.

Additionally, regulatory pressure on ingredient transparency is reshaping portfolios toward safer, traceable actives. This compliance-driven evolution builds trust, invites new users into medicated and cosmetic segments, and widens price ladders. Together, these forces are positioning scalp care as a long-term, data-informed growth engine within global beauty and personal care.

Key Takeaways

- The Global Anti-Dandruff Shampoos Market is projected to reach USD 12.4 Billion by 2034, growing from USD 6.8 Billion in 2024 at a CAGR of 6.2%.

- In 2024, Cosmetic Shampoo dominated the market By Product Type, holding a 54.2% share driven by premium appeal and lifestyle marketing.

- In 2024, Normal Hair segment led the By Hair Type analysis with a 33.4% share, supported by its universal suitability.

- In 2024, Liquid shampoos accounted for a 57.5% share in the By Form category, favored for their ease of use and familiarity.

- In 2024, Women emerged as the leading End User, capturing a 49.9% share, fueled by rising focus on scalp health and aesthetics.

- In 2024, Supermarkets & Hypermarkets led the Distribution Channel segment with a 38.6% share, driven by high product visibility and promotions.

- North America dominated the global market in 2024 with a 45.9% share, valued at USD 3.1 Billion, owing to strong awareness and purchasing power.

Market Segmentation Overview

Cosmetic Shampoos command leadership at 54.2%, propelled by fragrance-forward, gentle formulations, and sustained marketing. Meanwhile, Natural/Organic lines scale rapidly as clean-beauty preferences intensify. Medicated offerings retain a crucial role for persistent conditions, leveraging antifungal actives and dermatologist endorsements to secure trust among clinical and performance-centric users.

Across Hair Type, Normal Hair leads with 33.4% due to universal tolerance and climate versatility. Oily Hair solutions meet urban consumers’ sebum-control needs, while Dry & Flaky variants emphasize barrier repair. Color-Treated Hair SKUs protect vibrancy with sulfate-free, UV-shielding systems, merging cosmetic care and therapeutic control in one regimen.

By Form, Liquids dominate at 57.5% for familiarity and easy application across mass and professional channels. Gels attract younger shoppers with transparent aesthetics; creams deliver rich nourishment for dryness-prone scalps. Foams introduce quick-rinse convenience, and bar or powder formats address zero-waste preferences and travel-friendly routines.

By End User, Women lead at 49.9%, reflecting higher personal-care spend and loyalty to targeted solutions. Men’s segment accelerates through dual-benefit claims, notably anti-dandruff plus anti-hair fall. Unisex ranges streamline household purchasing, expanding penetration via balanced formulas suitable for all hair types and daily use.

By Distribution Channel, Supermarkets & Hypermarkets front-run at 38.6% on visibility and promotions. E-commerce surges on reviews, personalization, and delivery. Pharmacies & Drugstores anchor medicated trust, while Salons elevate premium therapies and regimen coaching. Other channels—including convenience and direct-selling—extend reach into rural and value-driven niches.

Drivers

First, rising consumer literacy on scalp microbiome balance and hygiene is elevating anti-dandruff from episodic remedy to preventive routine. Educational campaigns, derm partnerships, and clinical claims encourage regular usage patterns. As a result, shoppers trade up to proven actives while expecting sensorially appealing, irritation-minimizing bases.

Second, digital commerce and data-driven engagement are reshaping discovery and loyalty. Robust D2C storefronts, marketplace assortments, and subscription replenishment reduce friction and stockouts. Layered with AI consultation and content, brands can tailor regimens by hair type, climate, and sensitivity, lifting conversion, LTV, and cross-sell into conditioners and tonics.

Use Cases

Clinically managed regimens target seborrheic dermatitis, recurring flaking, and scalp itch using antifungal agents and barrier-support actives. Dermatologist-recommended SKUs fit weekly maintenance or flare-up protocols, reducing relapse and improving adherence through clear instructions, compatible conditioners, and scalp serums.

Lifestyle-oriented routines blend cosmetic freshness with prevention. For humidity-prone commuters or athletes, deep-cleansing yet gentle formulas manage sebum, odor, and buildup without stripping color or moisture. Multi-benefit daily shampoos—anti-dandruff plus smoothing or volumizing—simplify care for time-pressed consumers and shared households.

Major Challenges

Consumer skepticism toward harsh synthetics dampens demand for legacy formulations. Concerns around irritation, dryness, or long-term exposure push users toward sulfate-free, paraben-free, and fragrance-moderated options. Brands must reformulate without compromising efficacy, preserving foam quality and rinse feel while proving clinical parity.

Input-cost volatility and regulatory shifts complicate portfolio and pricing. Active ingredients—from zinc pyrithione to ketoconazole—face stricter oversight in select markets, prompting reformulation, new stability testing, and relabeling. Cost pass-through risks price elasticity; therefore, procurement agility and tiered innovation pipelines are essential to protect margins.

Business Opportunities

Natural and Ayurvedic expansions unlock new cohorts seeking gentle efficacy via neem, tea tree, salicylic acid alternatives, and soothing botanicals. Pairing these with dermatology-grade testing bridges clinical credibility and clean-beauty expectations, supporting premium pricing and broader retail placement from pharmacies to specialty beauty.

Personalization at scale offers defensible differentiation. AI scalp scans, climate-aware recommendations, and cadence-optimized subscriptions raise satisfaction and continuity. Bundled systems—shampoo, scalp tonic, weekly mask—create regimen stickiness, while refillable packaging and concentrated formats meet sustainability mandates and lower lifetime shipping footprints.

Regional Analysis

North America leads with 45.9% share valued at USD 3.1 Billion in 2024, buoyed by high awareness, dermatologist access, and willingness to pay for premium and medicated solutions. Omnichannel strength—mass retail, pharmacies, professional salons, and e-commerce—sustains category visibility and promotional intensity.

Europe advances through eco-certifications, stringent cosmetics regulations, and preference for mild, proven actives across Germany, France, and the U.K. Asia Pacific accelerates on urbanization, humidity-driven incidence, and hybrid demand for herbal-science blends in China, Japan, and South Korea. MEA and Latin America expand steadily via pharmacy trust and affordable mass options.

Recent Developments

- In August 2025, Olaplex acquired Boston-based biotech Purvala Bioscience to bolster bio-inspired molecule R&D and scalp-health innovation.

- In July 2025, L’Oréal acquired Color Wow, strengthening its Professional Hair Products portfolio and premium salon footprint.

- In May 2025, CLEAR (Unilever) launched “scalpceutical” anti-dandruff shampoos featuring selenium disulfide and patented technologies targeting clinical efficacy.

- In late 2024, CeraVe debuted its first anti-dandruff line in the U.S., combining hydration and barrier-support ingredients with dermatology-led positioning.

Conclusion

The Anti-Dandruff Shampoos Market is poised for durable, innovation-led growth—scaling from USD 6.8 Billion in 2024 to USD 12.4 Billion by 2034 at 6.2% CAGR. Brands that harmonize clinical efficacy, clean formulation, and personalized digital journeys will outpace the category, converting episodic problem-solvers into loyal, high-value regimen users across channels and regions.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)