Table of Contents

Overview

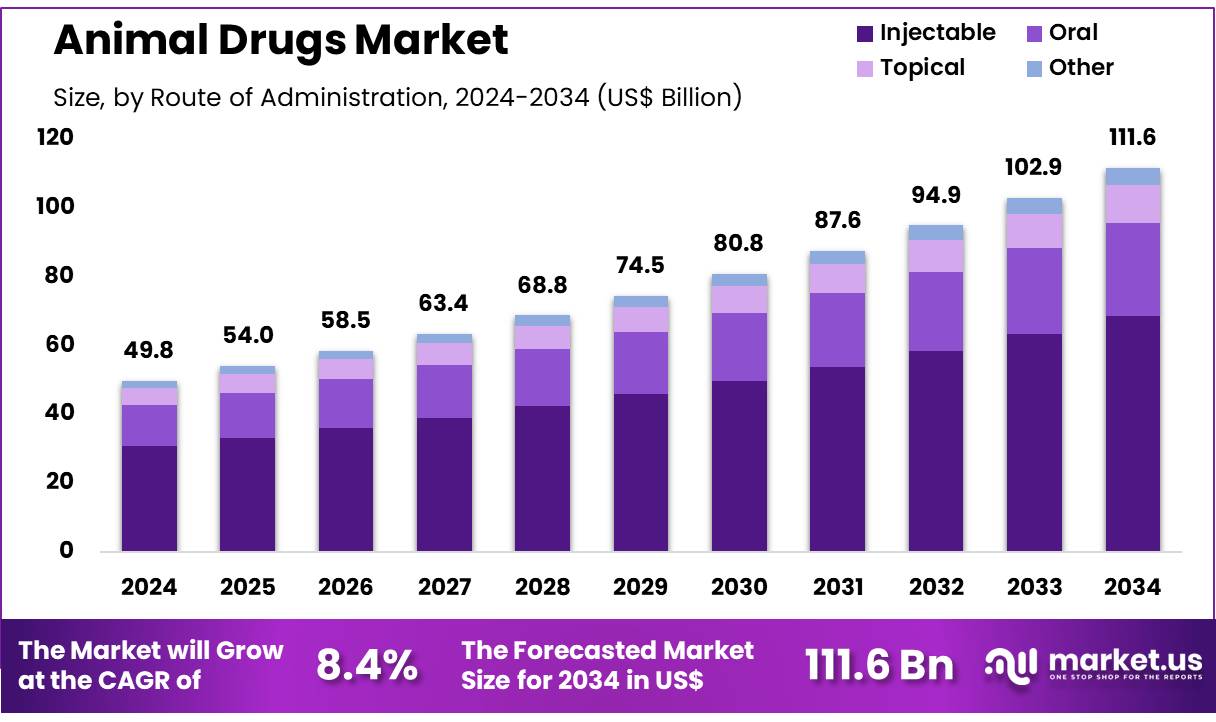

New York, NY – Nov 25, 2025 – Global Animal Drugs Market size is expected to be worth around US$ 111.6 billion by 2034 from US$ 49.8 billion in 2024, growing at a CAGR of 8.4% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 41.3% share with a revenue of US$ 20.6 Billion.

The global animal drugs market has been witnessing consistent expansion as veterinary healthcare demand continues to rise. The growth of the market can be attributed to the increasing prevalence of zoonotic diseases, expanding livestock populations, and the rising focus on companion animal health. Strong emphasis on preventive care and the adoption of advanced therapeutics have further supported market development across major regions.

Market revenue has been supported by sustained investment in research and development activities, enabling the introduction of improved pharmaceuticals, vaccines, and medicated feed additives. Regulatory approvals for new drug formulations have contributed to an accelerated pace of commercialization, thereby enhancing product availability in both developed and emerging economies.

The expansion of the companion animal segment has been driven by increasing pet ownership and the growing trend of premium veterinary services. Significant demand for anti-infectives, parasiticides, and anti-inflammatory drugs has been observed across clinics and veterinary hospitals. In livestock applications, productivity enhancement and disease management continue to be key market drivers.

The market outlook remains positive as biotechnology advancements and precision veterinary medicine gain momentum. Strategic collaborations between manufacturers and research institutions are expected to strengthen the development pipeline and improve treatment outcomes. North America and Europe remain major contributors to global revenue, while Asia-Pacific is projected to exhibit robust growth due to increasing commercial farming activities.

Key Takeaways

- In 2024, the animal drugs market generated revenue of US$ 49.8 billion, advancing at a CAGR of 8.4%, and the market value is projected to reach US$ 111.6 billion by 2033.

- The product type segment comprises biologics, pharmaceuticals, and medicated feed additives, with pharmaceuticals accounting for the largest share at 55.2% in 2024.

- Based on route of administration, the market is categorized into oral, injectable, topical, and others, where injectable formulations held a dominant share of 61.5%.

- In terms of animal type, the market is divided into production animals and companion animals, with production animals representing the largest segment at 62.8%.

- The distribution channel segment includes veterinary hospitals & clinics, e-commerce, offline retail stores, and others, and veterinary hospitals & clinics led the market with a 58.7% revenue share.

- North America emerged as the leading regional market, securing a 41.3% share in 2024.

Regional Analysis

North America Leading the Animal Drugs Market

North America accounted for the largest share of 41.3% in the animal drugs market, supported by rising pet healthcare expenditure, expanding livestock production, and an increasing number of regulatory approvals for advanced therapeutics. Spending on veterinary care in the United States exceeded US$ 38 billion in 2024, up from US$ 34 billion in 2022, as reported by the American Pet Products Association (APPA). This increase reflected stronger demand for pharmaceuticals and preventive treatments. According to the USDA, cattle and poultry production recorded a 5% rise in 2024 compared to 2022, driving higher consumption of antibiotics and vaccines.

Regulatory activity also strengthened market performance. The U.S. FDA’s Center for Veterinary Medicine approved 15% more new animal drug applications in 2023 relative to the previous year, improving access to innovative products. Zoetis reported an 8% increase in revenue in 2023, supported by sustained demand for parasiticides and biologics. In Canada, the Canadian Animal Health Institute (CAHI) reported higher antimicrobial sales for livestock in 2024 due to broader disease prevention efforts. These combined developments contributed to steady regional growth.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to expand at the fastest CAGR due to the rapid development of livestock sectors, increasing rates of pet ownership, and supportive government initiatives. India vaccinated more than 300 million livestock in 2023 under the National Animal Disease Control Programme, contributing to rising drug utilization.

China’s Ministry of Agriculture and Rural Affairs approved a higher number of veterinary drugs in 2024 compared to 2022, facilitating the introduction of new treatments. Japan’s growing pet population continued to strengthen demand for companion animal medicines. Australia allocated US$ 50 million in 2024 to enhance livestock biosecurity, further stimulating pharmaceutical requirements. These factors collectively indicate strong growth prospects for the region, supported by innovation and policy-driven advancements.

Emerging Trends

- Regulatory Modernization and Process Reorganization: In October 2024, a major reorganization was initiated within the FDA’s Center for Veterinary Medicine to modernize the structure of animal drug evaluation offices. The initiative has been designed to streamline review workflows, lessen administrative complexity, and accelerate the introduction of safe and effective veterinary therapies.

- Heightened Focus on Antimicrobial Stewardship: A new antimicrobial stewardship plan covering FY 2024–2028 has been introduced to strengthen responsible drug use in veterinary practice. The strategy advances previous efforts by promoting stewardship-aligned drug administration, supporting stewardship adoption across clinical settings, and improving national monitoring of antimicrobial resistance and use trends.

- Declining Use of Medically Important Antimicrobials: Sales and distribution of medically important antimicrobials for food-producing animals declined by 2 percent, falling from 6.25 million kg in 2022 to 6.13 million kg in 2023. This change represents a 37 percent reduction from the 2015 peak, indicating widespread adoption of stewardship initiatives across livestock systems.

- Diversification of Veterinary Biologics: Veterinary biologics are expanding, supported by the licensing of novel products such as monoclonal antibodies and RNA-based therapies by USDA APHIS. A monoclonal antibody targeting canine atopic dermatitis, granted under CVB license VLN 190, demonstrates rising interest in targeted immunotherapies for companion animals.

Use Cases

- Controlling Bacterial Infections in Food Animals: In 2023, approximately 6,127,991 kg of medically important antibiotics were sold for use in cattle, swine, poultry, and other food-producing species. These drugs were utilized to prevent and manage respiratory, gastrointestinal, and systemic infections, supporting herd health and sustaining agricultural productivity.

- Vaccination Against Highly Pathogenic Avian Influenza (HPAIV): More than 90 million domestic birds across 49 States were impacted by HPAIV during FY 2024. Research efforts by USDA-ARS have focused on advancing rapid-onset vaccine technologies and refining diagnostic tools to strengthen prevention and outbreak containment in poultry production systems.

- Targeted Immunotherapy in Companion Animals: A licensed monoclonal antibody product (VLN 190) is being employed to treat canine atopic dermatitis, a chronic dermatological condition affecting up to 10 percent of dogs. The therapy offers a targeted immunologic approach that may reduce dependence on broad-spectrum immunosuppressants and improve overall patient outcomes.

Frequently Asked Questions on Animal Drugs

- How are animal drugs classified?

Animal drugs are classified into antiparasitics, anti-infectives, anti-inflammatory agents, vaccines, and hormonal products. This classification is based on therapeutic application, targeted disease area, and species-specific usage requirements established under veterinary healthcare standards. - How is the safety of animal drugs ensured?

Safety is ensured through rigorous preclinical studies, controlled clinical trials, and regulatory review processes. Post-market surveillance systems are employed by authorities to monitor adverse effects and ensure that products maintain consistent efficacy and safety across diverse animal populations. - Why are animal drugs important?

Animal drugs support livestock productivity, reduce disease burden, and improve companion animal welfare. Their utilization contributes to food security by maintaining healthy herds, while also enabling veterinarians to manage and control infectious diseases effectively in various animal production systems. - What regulations govern animal drugs?

Regulations are enforced by national authorities such as the FDA, EMA, and other veterinary regulatory bodies. These frameworks define approval processes, manufacturing standards, residue limits, and monitoring systems designed to ensure product safety, quality, and compliance. - What is driving growth in the animal drugs market?

Market growth is driven by rising pet ownership, increased livestock disease prevalence, and expanding demand for high-quality animal protein. Investments in veterinary healthcare and advancements in biotechnology further contribute to sustained market expansion across global regions. - Which segments dominate the animal drugs market?

Pharmaceuticals, vaccines, and medicated feed additives dominate the market. Companion animal drugs exhibit stronger growth due to rising spending on pet health, while livestock-focused products maintain significant demand linked to commercial farming and food production requirements. - Which regions lead the animal drugs market?

North America and Europe lead due to advanced veterinary healthcare systems, strong regulatory frameworks, and high expenditure on companion animal treatment. Rapid growth is observed in Asia-Pacific, driven by expanding livestock production and rising consumer awareness.

Conclusion

The animal drugs market continues to demonstrate stable and sustained expansion, supported by rising veterinary healthcare needs across both companion and production animals. Market performance has benefited from strong R&D investments, increasing regulatory approvals, and growing emphasis on preventive care.

Demand for pharmaceuticals, biologics, and advanced therapeutics remains high as livestock productivity and pet ownership increase globally. North America maintains a leading position, while Asia-Pacific is projected to achieve the fastest growth due to structural industry developments and government-led disease control initiatives. Overall, biotechnology advancements and evolving stewardship practices are expected to reinforce future market progression.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)