Table of Contents

Overview

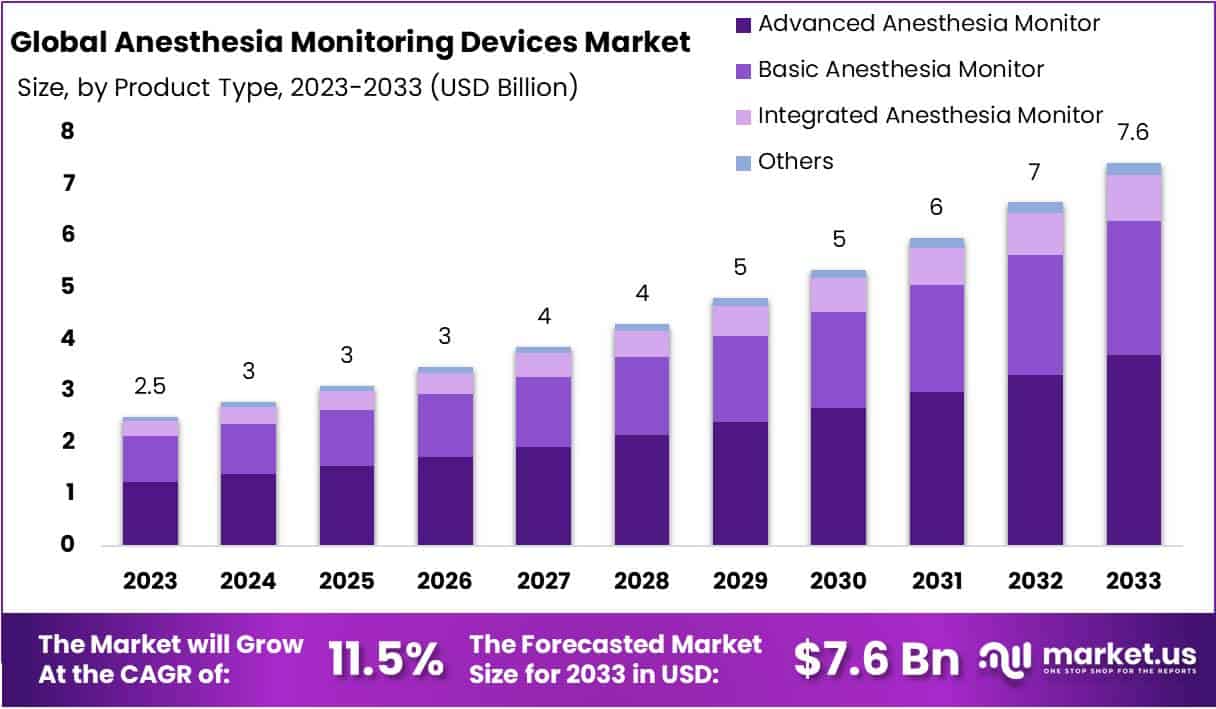

The global anesthesia monitoring devices market is projected to reach USD 7.6 billion by 2033, rising from USD 2.5 billion in 2023. This growth is supported by an expanding surgical workload worldwide. The increasing volume of cardiovascular, orthopedic, neurological, and trauma procedures has resulted in sustained demand for advanced monitoring solutions. The aging population continues to contribute to higher surgical intervention rates, which has reinforced the need for precise perioperative monitoring. As healthcare systems manage more complex cases, the deployment of modern, efficient anesthesia monitoring technologies has become essential to support clinical decision-making and patient stability during procedures.

The growing establishment of integrated operating rooms has contributed to wider adoption of multi-parameter monitoring systems. Upgrades to hospital infrastructures have been associated with increased use of devices capable of real-time data tracking and automated measurements. The need for seamless information flow during surgeries has encouraged healthcare facilities to invest in unified operating room technologies. This trend has strengthened the demand for anesthesia monitoring platforms that enhance operational efficiency. As surgical environments become more technology-driven, systems offering comprehensive and synchronized monitoring capabilities are being prioritized for new installations and equipment replacements.

Technological progress has further accelerated market expansion. Advancements in sensor accuracy, wireless communication, and data analytics have enabled development of next-generation monitoring tools. Innovations such as depth-of-anesthesia monitors, enhanced capnography devices, and non-invasive measurement solutions have improved patient assessment and clinical outcomes. These improvements have been aligned with regulatory expectations for standardized monitoring practices. As perioperative teams seek tools that support safer surgical processes, the adoption of devices with advanced diagnostic features has increased across hospitals and surgical centers.

Rising attention to patient safety has encouraged wider integration of continuous monitoring throughout the perioperative pathway. Guidelines issued by regulatory bodies have emphasized the importance of consistent physiological tracking to reduce surgical risks. This focus has strengthened the use of devices that support immediate detection of complications and refine anesthesia delivery. The demand has been sustained by the need to improve outcome reliability and ensure adherence to quality-of-care standards. As healthcare systems prioritize risk mitigation, the uptake of technologically advanced anesthesia monitors has continued to gain momentum.

Increasing healthcare expenditure in emerging economies has contributed to higher adoption of monitoring systems. Investments in hospital expansion, modernization of surgical departments, and government-led initiatives to enhance surgical care have supported market growth. Additionally, the rising volume of minimally invasive procedures has created demand for high-performance, real-time monitoring capabilities. Growth in outpatient and ambulatory surgical centers has further encouraged procurement of compact and cost-effective monitoring devices. The increasing prevalence of chronic diseases such as cancer and cardiovascular disorders has added to the global surgical burden, supporting sustained demand for anesthesia monitoring technologies.

Key Takeaways

- The global anesthesia monitoring devices market is projected to reach USD 7.6 billion by 2033, driven by an 11.5% CAGR from its 2023 valuation.

- Advanced anesthesia monitors accounted for 49.8% of total product-based revenue in 2023, reflecting strong adoption of enhanced monitoring technologies across clinical settings.

- Hospitals captured 85.2% of end-use demand due to established healthcare infrastructure and the presence of skilled clinicians supporting advanced anesthesia monitoring practices.

- Rising prevalence of chronic diseases and ongoing technological improvements in anesthesia monitoring have been observed to accelerate market expansion across major regions.

- Market growth is expected to face constraints because of adverse effects associated with anesthesia administration, creating concerns among patients and healthcare providers.

- North America held a leading 45.6% share in 2023, supported by strong healthcare investment and early adoption of advanced anesthesia monitoring systems.

Regional Analysis

North America was identified as the leading region in the anesthesia monitoring devices market in 2023. The region accounted for a significant share of 45.6 percent. The regional dominance has been attributed to the rising burden of chronic diseases. Higher cases of cardiovascular disorders, cancer, and obesity have increased the number of surgical procedures. This trend has supported the higher adoption of anesthesia monitoring systems. The overall demand has been strengthened by advanced healthcare infrastructure and strong investments in perioperative care technologies.

The prevalence of cardiovascular diseases has played a major role in supporting regional growth. A notable increase in cardiac surgeries has been observed. Cedars-Sinai reported that coronary artery bypass graft procedures remain the most common heart surgeries in the United States. More than 300,000 bypass surgeries are performed each year. This consistent surgical volume has supported the use of anesthesia monitoring devices. Hospitals and surgical centers have increased reliance on precision monitoring to ensure patient safety and procedural accuracy.

Incidence rates of heart attacks have further contributed to the need for reliable anesthesia monitoring technologies. Data from the Centers for Disease Control and Prevention indicated that a heart attack occurs every 40 to 45 seconds in the country. This reflects nearly 805,000 individuals affected each year. Such high disease occurrence has resulted in greater hospitalization and surgical intervention rates. As a result, the adoption of anesthesia monitoring devices has expanded. Clinical settings have emphasized equipment that supports effective intraoperative management and postoperative stability.

Segmentation Analysis

The market for anesthesia monitoring devices has been led by advanced anesthesia monitors. This category accounted for a 49.8 percent share in 2023. The segment includes standalone capnography systems, gas monitors, and MRI compatible units. The growth of this category has been linked to steady technological advancements in monitoring systems. Increased precision, durability, and digital integration have improved product performance. Strong innovation supported by manufacturers has further strengthened the segment. These improvements have positioned advanced systems as the preferred choice in critical care settings.

The expansion of advanced anesthesia monitors has also been supported by rising investments in research and development. Government expenditure has increased, with funds directed toward next-generation medical technologies. Industry players have boosted innovation pipelines to meet evolving clinical needs. A notable example is the launch of the MAGLIFE RT-1 MRI compatible monitor by Schiller in April 2022. The system enables detailed patient tracking during MRI procedures. It can be fully operated from outside the Faraday cage. Such developments indicate sustained momentum in the segment.

The end user landscape shows clear dominance of the hospital segment. Hospitals captured 85.2 percent of the market in 2023. This leadership has been attributed to strong infrastructure availability and the presence of skilled professionals. Hospitals maintain higher adoption rates due to their capacity to manage complex procedures. Their ability to integrate advanced monitoring systems supports continued demand. The market position of hospitals is expected to remain strong. Their operational scale and equipment investments contribute to ongoing uptake of anesthesia monitoring technologies.

Ambulatory surgical centers have captured a notable market share and are positioned for further growth. These centers have increased in number and serve as key sites for non-operating room anesthesia. They often provide faster and more cost-efficient outpatient care compared to hospitals. This advantage supports demand for reliable anesthesia systems. According to MedPac, the number of such centers rose by 1.9 percent in 2014 compared with 2013. Continued expansion of these facilities is expected to support broader adoption of monitoring devices across outpatient settings.

Market Key Segments

By Product Type

- Advanced Anesthesia Monitor

- Basic Anesthesia Monitors

- Integrated Anesthesia Monitors

- Other

By End Use

- Hospitals

- Ambulatory Surgical Centers

- Others

Key Players Analysis

The competitive structure of the anesthesia monitoring devices market is shaped by a steady rise in strategic activities aimed at strengthening operational capabilities. Continuous investments in technology advancement have supported the development of high-precision monitoring systems. This approach has enabled leading companies such as BPL Medical Technologies, Dragerwerk AG & Co., and Heyer Medical AG to reinforce their product pipelines. Their efforts have been directed toward improving accuracy, safety, and real-time monitoring performance, which has supported stable market growth and enhanced clinical adoption across healthcare facilities.

Product innovation remains a central strategy as manufacturers expand research efforts to introduce advanced monitoring solutions. The growing focus on non-invasive and patient-centric technologies has encouraged firms including Masimo, Medasense Biometrics Ltd, and Shenzhen Mindray Bio-Medical Electronics Co., Ltd to diversify portfolios. These players have emphasized sensor accuracy, data connectivity, and integration with hospital systems. Their sustained R&D investment has improved product efficiency, strengthened brand visibility, and supported broader global reach.

Collaborations and partnerships have played a crucial role in enhancing distribution channels and accelerating product development. Companies such as Neurowave Systems, Inc., Nonin, and Veterinary Anesthesia Systems, Inc. have utilized cooperative agreements to expand market access. These alliances have enabled them to share technological capabilities, improve device performance, and address emerging clinical demands. Increased collaborative efforts have also supported consistent product updates, strengthening their ability to compete in both developed and emerging healthcare markets.

Mergers and regional expansion strategies have contributed to improved competitive positioning among global manufacturers. Firms including Allied Biotech Corporation, FUKUDA DENSHI, and Schiller Americas have focused on acquiring complementary technologies and expanding operational footprints. Their initiatives have strengthened supply capabilities, improved customer engagement, and supported the introduction of value-added product lines. This strategic alignment has contributed to market consolidation while enabling these companies to maintain strong, long-term growth prospects within the anesthesia monitoring devices market.

Top Key Players in the Anesthesia Monitoring Devices Market

- BPL Medical Technologies

- Dragerwerk AG & Co.

- Heyer Medical AG

- Masimo

- Medasense Biometrics ltd

- Shenzhen Mindray Bio-Medical Electronics Co., ltd

- Neurowave Systems, Inc.

- Nonin

- Veterinary Anesthesia Systems, Inc.

- Allied Biotech Corporation

- FUKUDA DENSHI

- Schiller Americas

Challenges

1. High Cost of Advanced Monitoring Systems

The high cost of advanced anesthesia monitors remains a major barrier. These systems include integrated modules, sensors, and software that increase overall expenses. Maintenance also adds to the financial burden. Many hospitals with limited budgets postpone upgrades or avoid purchasing new devices. Small clinics and facilities in developing markets face the same issue. As a result, adoption of modern anesthesia monitoring solutions continues to grow at a slower pace.

2. Limited Access in Low-Resource Settings

Access to modern anesthesia monitoring devices is still limited in many low-resource regions. Several healthcare centers depend on outdated or basic systems. Investment in perioperative care infrastructure remains low. This gap restricts the use of advanced monitoring solutions during surgeries. Rural hospitals also struggle with procurement challenges. As a result, the quality of patient monitoring varies widely. These limitations slow down improvements in overall surgical safety and clinical outcomes.

3. Need for Skilled Healthcare Professionals

Advanced anesthesia monitors require trained professionals for safe and accurate use. Many healthcare systems face shortages of anesthesiologists and qualified technicians. This lack of skilled staff limits the proper handling of monitoring devices. Even when advanced systems are installed, they may not be used to their full capability. Inexperienced personnel may struggle with calibration, interpretation, or troubleshooting. These skill gaps reduce the effectiveness of modern anesthesia monitoring technologies.

4. Device Integration and Interoperability Issues

Hospitals often use medical devices from multiple manufacturers. Integrating these systems with electronic health records and surgical platforms becomes difficult. In many cases, there is no common standard for data exchange. This creates workflow inefficiencies during surgical procedures. Interoperability gaps also affect real-time data sharing, which is essential for clinical decision making. As a result, hospitals experience delays, errors, or manual workarounds. These issues affect overall efficiency in anesthesia monitoring.

5. Regulatory and Compliance Requirements

Anesthesia monitoring devices must comply with strict regulatory standards. Approval processes are long and require detailed clinical validation. Manufacturers must invest significant time and resources to meet regional compliance rules. These requirements slow the launch of new products into the market. Companies also face varying regulations across regions, which increases complexity. As a result, innovation cycles become longer. The need for constant documentation and audits adds additional operational pressure.

6. Risk of Technical Failures

Technical failures in anesthesia monitoring devices present safety risks during surgical procedures. Regular calibration and maintenance are required to ensure accuracy. Hospitals must invest in service contracts, system checks, and user training. Unexpected failures can interrupt surgeries or create delays. In many facilities, aging equipment increases the likelihood of malfunction. These risks lead to greater operational costs. Consistent monitoring and support are needed to maintain device reliability and patient safety.

Opportunities

1. Increasing Number of Surgeries

The global rise in surgical procedures is creating strong demand for anesthesia monitoring devices. More elderly individuals and a growing burden of chronic diseases have increased the need for safe and effective surgical care. As a result, hospitals are adopting advanced monitoring systems to manage patients more efficiently. The continued rise in complex and routine surgeries is expected to sustain long-term growth in this market.

2. Rising Use of Minimally Invasive Procedures

Minimally invasive surgeries are becoming more common because they reduce recovery time and complications. These procedures require accurate, real-time monitoring to maintain patient safety. The need for continuous data during surgery is increasing the use of anesthesia monitoring devices across hospitals and surgical centers. The shift toward safer and less invasive operations is expected to drive consistent demand for these systems in the coming years.

3. Advances in Monitoring Technologies

New technologies in sensors, analytics, and wireless systems are improving the efficiency of anesthesia monitoring devices. The use of AI is helping clinicians receive faster and more accurate insights during surgery. These advancements support better decision-making and enhance patient safety. Real-time data visualization is also improving the quality of care. As more hospitals adopt smart and integrated solutions, the market is expected to experience notable growth.

4. Expansion of Healthcare Infrastructure in Emerging Markets

Emerging economies are investing heavily in hospitals, surgical units, and intensive care facilities. These improvements are increasing access to modern perioperative care. Governments are prioritizing healthcare upgrades, which is raising demand for advanced monitoring systems. New surgical centers and expanding healthcare coverage are also supporting market growth. As countries strengthen their medical infrastructure, adoption of anesthesia monitoring devices is expected to rise steadily.

5. Growing Preference for Patient Safety and Quality Care

Healthcare providers are placing greater emphasis on reducing risks and improving patient outcomes. Continuous monitoring is viewed as essential for maintaining safety during surgery. Hospitals are adopting advanced systems to ensure accurate assessment of patient status. This focus on safety and quality care is creating strong demand for reliable anesthesia monitoring devices. As expectations for better care increase, the market is likely to expand further.

6. Increasing Adoption of Portable and Wearable Devices

Portable anesthesia monitoring devices are becoming popular due to their flexibility in emergency and transport settings. These compact systems support continuous observation in diverse clinical environments. Their ease of use and mobility make them valuable for critical care teams. As healthcare providers seek more adaptable solutions, demand for portable and wearable monitors is rising. This trend is expected to boost market opportunities for manufacturers.

7. Integration of Digital Health and Connectivity

Digital health integration is transforming anesthesia monitoring systems. Devices that connect with hospital information systems and cloud platforms allow remote monitoring and automated data capture. This improves workflow and ensures accurate documentation. Connected care models support better decision-making and enhance patient management. As hospitals move toward digital environments, demand for integrated and connected monitoring solutions is expected to grow steadily.

Conclusion

The anesthesia monitoring devices market is expected to grow steadily as surgical procedures increase worldwide and healthcare systems adopt more advanced technologies. The demand for safe and efficient patient monitoring has been supported by rising chronic diseases, aging populations, and the expansion of modern operating rooms. Progress in sensor technology, data integration, and non-invasive tools has strengthened product performance and improved clinical decision making. Growth is also encouraged by investments in healthcare infrastructure across developing regions. Although challenges such as high device costs and limited access in some areas remain, ongoing innovation and a stronger focus on patient safety are expected to support sustained market expansion over the coming years.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)