Table of Contents

Overview

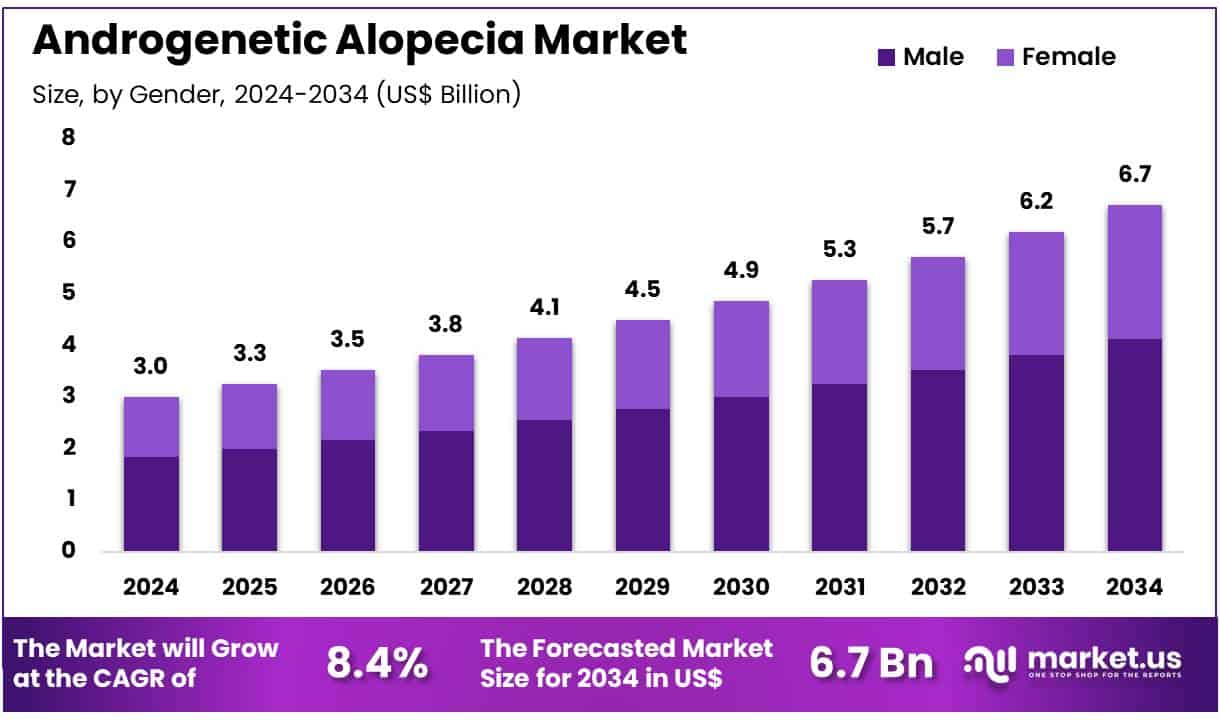

New York, NY – June 23, 2025 – Global Androgenetic Alopecia Market size is expected to be worth around US$ 6.7 billion by 2034 from US$ 3.0 Billion in 2024, growing at a CAGR of 8.4% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.4% share with a revenue of US$ 1.2 Billion.

The global androgenetic alopecia market is experiencing steady growth, driven by the increasing prevalence of hair loss among both men and women, particularly those aged 30 and above. Androgenetic alopecia, also known as male-pattern or female-pattern baldness, is the most common form of progressive hair loss caused by genetic and hormonal factors. It affects over 50% of men and nearly 40% of women by the age of 50, according to data from leading public health agencies.

The market is segmented based on treatment type, gender, and end-user. Pharmacological treatments such as topical minoxidil and oral finasteride remain the primary options, while demand for advanced therapies like platelet-rich plasma (PRP), low-level laser therapy (LLLT), and stem cell-based interventions continues to grow. In 2023, male patients accounted for a dominant share, but awareness and diagnosis among female patients are increasing rapidly.

Clinics specializing in dermatology and aesthetic medicine represent the largest end-user segment, benefiting from the rising number of outpatient consultations for hair restoration. North America holds a significant share due to better diagnosis rates, treatment availability, and consumer awareness. However, Asia-Pacific is expected to witness the highest growth rate, supported by a growing youth population, urbanization, and rising cosmetic consciousness.

Key Takeaways

- In 2023, the global androgenetic alopecia market generated revenue of approximately US$ 3.0 billion and is projected to reach US$ 6.7 billion by 2033, growing at a compound annual growth rate (CAGR) of 8.4% over the forecast period.

- By gender, the male segment accounted for the largest market share at 61.5% in 2023, reflecting the higher prevalence of pattern baldness among men.

- In terms of treatment type, the market is categorized into pharmaceuticals and devices. Pharmaceuticals dominated the market in 2023, representing 58.3% of the total revenue, owing to widespread usage of approved topical and oral medications.

- Based on end-use, dermatology clinics emerged as the leading segment, capturing a revenue share of 62.0%. This dominance is attributed to the availability of specialized treatments and professional medical supervision in clinical settings.

- The sales channel segment is classified into prescription-based and over-the-counter (OTC) distribution. The prescription segment led the market in 2023 with a 55.2% share, indicating a strong preference for medically guided treatment approaches.

- Regionally, North America held the largest share of the global market, accounting for 38.4% in 2023. This leadership is supported by high awareness, established dermatology infrastructure, and increasing adoption of advanced hair loss treatments.

Segmentation Analysis

- Gender Analysis: In 2023, the male segment dominated the androgenetic alopecia market with a 61.5% share. This growth is driven by the high prevalence of male pattern baldness, influenced by genetic factors, stress, and lifestyle changes. Increasing awareness and adoption of hair loss treatments among men, along with the rise in grooming and self-care trends, are expected to sustain the segment’s growth. The market is likely to benefit from expanding product lines specifically targeting male consumers.

- Treatment Analysis: Pharmaceutical treatments captured a 58.3% market share in 2023, owing to the proven efficacy of drugs like finasteride and dutasteride in treating androgenetic alopecia. These medications work by reducing dihydrotestosterone (DHT) levels, a hormone responsible for hair loss. As research continues and new drug formulations are introduced, demand for pharmaceutical interventions is expected to rise. Their convenience and long-term benefits over topical products further enhance their appeal, supporting steady growth in the treatment segment.

- End-Use Analysis: Dermatology clinics accounted for the largest revenue share of 62.0% in 2023, driven by increasing patient preference for professional, clinical-grade treatments. Services such as PRP therapy, laser applications, and hair transplants are widely offered, ensuring reliable results. The expansion of specialized clinics and higher awareness of dermatological solutions are propelling demand. As consumers seek expert-guided treatments for hair loss, the segment is anticipated to maintain its dominant position in the end-use landscape.

- Sales Channel Analysis: The prescriptions segment secured a 55.2% share in 2023, reflecting the rising preference for clinically approved hair loss treatments. Finasteride and topical minoxidil remain prominent choices, prescribed frequently due to their effectiveness in slowing hair thinning and promoting regrowth. Increased consultations with healthcare professionals and better patient outcomes are fueling the shift toward prescription-based solutions. As awareness improves, this channel is expected to witness continued growth, driven by trust in regulated pharmaceutical options.

Market Segments

By Gender

- Male

- Female

By Treatment

- Pharmaceuticals

- Devices

By End-use

- Dermatology Clinics

- Homecare Settings

By Sales Channel

- Prescriptions

- OTC

Regional Analysis

North America Dominates the Androgenetic Alopecia Market

In 2023, North America led the androgenetic alopecia market, capturing the highest revenue share of 38.4%. This dominance is attributed to a growing patient base, increased treatment adoption, and continuous advancements in therapeutic options. Data from the National Institutes of Health (NIH) indicated that approximately 50 million men and 30 million women in the United States experienced pattern hair loss in 2023, an increase from the previous year.

The U.S. Food and Drug Administration (FDA) approved two new topical hair regrowth formulations in early 2024, enhancing treatment accessibility. Major pharmaceutical companies, including Pfizer and Eli Lilly, reported increased sales of finasteride and minoxidil products in their 2023 annual financial disclosures. Furthermore, the American Academy of Dermatology (AAD) documented a notable rise in patient consultations for hair loss treatments between 2022 and 2023.

In Canada, the Canadian Dermatology Association observed growing interest in platelet-rich plasma (PRP) therapies during 2023. Insurance coverage for FDA-approved treatments also expanded, supported by the Centers for Medicare & Medicaid Services (CMS) in late 2023, further accelerating market growth.

Asia Pacific Expected to Register the Fastest Growth Rate

The Asia Pacific region is projected to experience the highest compound annual growth rate (CAGR) during the forecast period. This expansion is driven by increasing disposable income, heightened aesthetic awareness, and advancements in healthcare infrastructure across key economies.

The Indian Journal of Dermatology reported a year-on-year rise in clinical consultations for hair loss in 2023. In early 2024, China’s National Health Commission (NHC) approved three new topical therapies, likely to improve treatment access. Japan’s Ministry of Health, Labour and Welfare (MHLW) recorded a significant increase in prescriptions for 5-alpha reductase inhibitors, indicating rising patient demand.

In South Korea, the national dermatological society reported a sharp increase in hair transplant procedures between 2022 and 2023. Meanwhile, Australia’s Therapeutic Goods Administration (TGA) fast-tracked approval of two novel treatments in 2023 to meet growing demand. Southeast Asian governments are investing more in dermatological research, with Thailand’s Ministry of Public Health allocating US\$10 million for hair loss research initiatives in 2024. Leading market players such as Merck and Johnson & Johnson are expected to increase their presence in the region, further supporting long-term market expansion.

Emerging Trends

- Targeted Molecular Pathways: The modulation of key signaling pathways has been identified as a promising direction for future therapies. Research has highlighted the Wnt/β-catenin cascade and androgen receptor (AR) axis as critical regulators of hair-follicle cycling. Novel agents aiming to activate Wnt signaling or inhibit AR interaction are under exploration, with preclinical studies suggesting potential to restore miniaturized follicles toward anagen (growth) phases.

- Stem Cell–Based Approaches: Autologous and allogeneic stem cell therapies are being advanced to promote follicular regeneration. Systematic reviews indicate that mesenchymal stem cells, including adipose-derived and hair-follicle derived populations, can secrete growth factors that enhance follicle viability. Early-phase clinical trials have demonstrated safety and preliminary efficacy in increasing hair density, warranting larger, controlled studies.

- Repurposed Low-Dose Oral Minoxidil: Low-dose oral minoxidil (0.25–5 mg/day) has gained traction as an off-label, systemic alternative to topical application. In one cohort, 90 % of male patients exhibited clinical improvement after six months of 5 mg daily dosing, with faster onset than traditional regimens. Side effects, such as hypertrichosis and edema, were dose-dependent and generally mild.

- Autologous and Minimally Invasive Modalities: Techniques such as platelet-rich plasma (PRP) injections, microneedling, and mesotherapy are being combined with existing pharmacotherapies to potentiate outcomes. A comprehensive evaluation noted an uptick in clinical adoption of PRP and microneedling protocols, driven by patient demand for minimally invasive options and preliminary data supporting follicular stimulation via growth-factor release.

Use Cases

- Oral Finasteride Therapy: In a large Japanese study of over 3 000 males, 11.1 % of participants experienced significant hair regrowth, 36.5 % had moderate improvement, and 39.5 % showed slight increases over three years of continuous finasteride use. Vertex (crown) regions responded more robustly than frontal areas.

- Low-Dose Oral Minoxidil: Administration of 5 mg daily oral minoxidil yielded significant increases in total hair counts at both 12 and 24 weeks in treated males. Ninety percent demonstrated clinical improvement, while approximately 25 % reported hypertrichosis, underscoring the importance of dose titration and monitoring.

- Platelet-Rich Plasma (PRP) Injections: In a one-year study, mean hair counts increased from baseline to 153.70 ± 39.92 follicular units per cm² after four monthly PRP sessions. Patient satisfaction averaged 7.1 out of 10, and adverse effects were minimal, supporting PRP as a viable adjunctive therapy.

- Microneedling Combined with Topical Agents: Clinical protocols integrating microneedling with minoxidil or PRP have been shown to enhance percutaneous drug delivery and follicular stimulation. Although quantitative data are still emerging, early trials indicate that combined regimens can yield faster and more pronounced increases in hair density compared to monotherapy.

Conclusion

The global androgenetic alopecia market is poised for robust growth, driven by rising prevalence, increasing treatment awareness, and expanding therapeutic innovations. With pharmaceuticals leading the treatment segment and dermatology clinics dominating end-use, demand is being propelled by clinically guided interventions.

North America currently holds the largest share, while Asia Pacific is set to witness the fastest growth due to favorable demographic and regulatory trends. Emerging therapies such as stem cell treatments, low-dose oral minoxidil, and PRP are reshaping the clinical landscape. As both male and female patients seek effective solutions, the market is expected to expand significantly through 2034.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)