Table of Contents

Overview

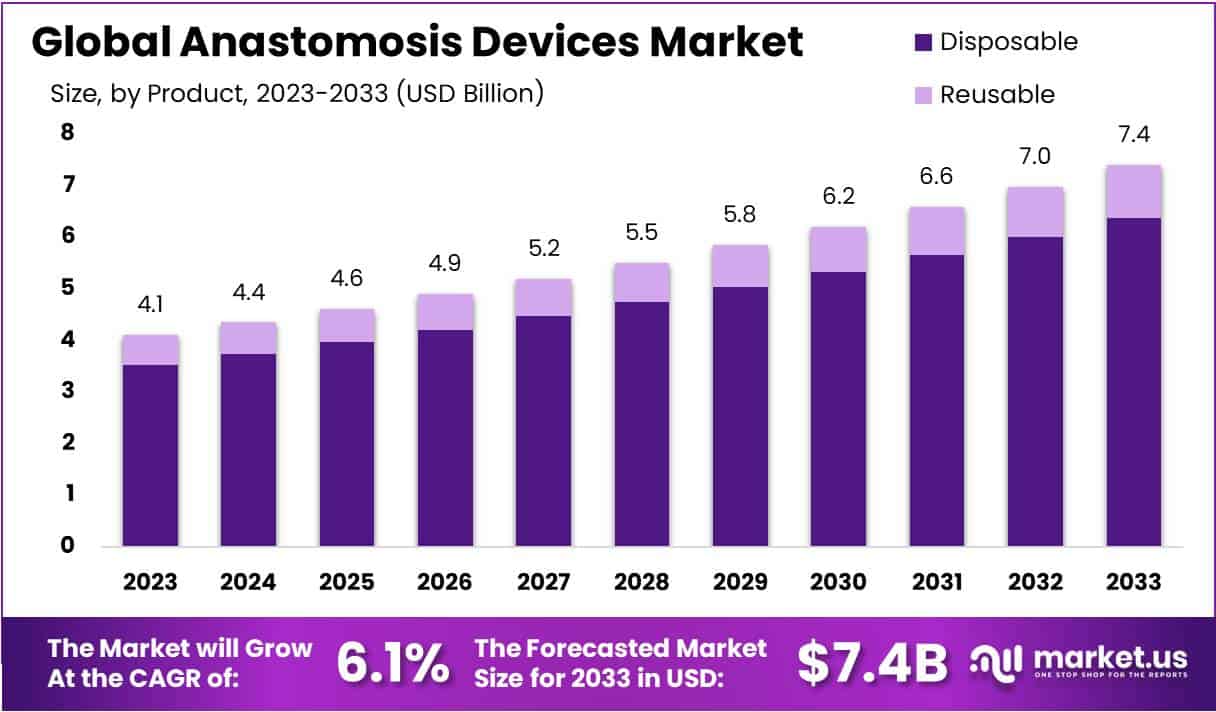

The Global Anastomosis Devices Market is projected to expand significantly, reaching USD 7.4 billion by 2033 from USD 4.1 billion in 2023. This growth represents a Compound Annual Growth Rate (CAGR) of 6.1% over the forecast period of 2024–2033. The market expansion is primarily driven by the rising prevalence of gastrointestinal cancers, inflammatory bowel disease, and cardiovascular conditions. These disorders frequently require surgical procedures such as colorectal surgeries, coronary artery bypass grafting, and bariatric surgeries. The growing patient pool undergoing such interventions continues to increase the demand for anastomosis devices.

Technological advancements are shaping the competitive landscape of this market. The development of automated suturing systems, minimally invasive stapling devices, and bioabsorbable materials has improved surgical precision and reduced operative time. These innovations are enhancing patient outcomes by minimizing post-operative complications and supporting faster recovery. Consequently, surgeons are increasingly preferring advanced anastomosis devices over traditional hand-sewn techniques. Continuous research and development by manufacturers is expected to accelerate the adoption of next-generation devices across hospitals and surgical centers.

The rising preference for minimally invasive and robotic-assisted surgeries is further propelling market growth. Procedures performed through laparoscopic or robotic systems reduce hospital stays, lower infection risks, and provide better cosmetic results. Anastomosis devices designed for compatibility with robotic platforms are anticipated to experience strong demand as robotic surgery penetration rises globally. This trend reflects the healthcare industry’s shift toward precision-driven solutions that offer both clinical and economic advantages.

The growing geriatric population represents another key driver. Elderly individuals are at higher risk of cardiovascular disease, gastrointestinal disorders, and cancer, all of which often necessitate surgical intervention. This demographic trend, coupled with increasing bariatric and organ transplant surgeries, is fueling device demand. Rising cases of obesity worldwide are contributing to the popularity of gastric bypass procedures, while liver and kidney transplants also rely heavily on efficient anastomosis solutions to ensure successful surgical outcomes.

Healthcare infrastructure development and increasing expenditure are creating a favorable environment for market expansion. Emerging economies are investing in modern hospitals and advanced surgical equipment, making specialized procedures more accessible. Additionally, strategic collaborations, mergers, and frequent product launches by leading companies are strengthening product portfolios and market reach. The introduction of safer, surgeon-friendly devices is expected to reinforce market adoption and support steady growth throughout the forecast period.

Key Takeaways

- The global Anastomosis Devices Market is expected to attain USD 7.4 billion by 2033, expanding steadily at a 6.1% CAGR.

- In 2023, disposable anastomosis devices dominated with an 86.4% share, owing to superior convenience, hygiene standards, and reduced infection risks during surgical interventions.

- Cardiovascular surgery accounted for 52% market share in 2023, reflecting the essential role of these devices in heart-related procedures and patient outcomes.

- Hospitals captured more than 58.6% share in 2023, reaffirming their reliance on these devices for complex surgical procedures and critical healthcare delivery.

- Rising surgical volumes, technological advancements, and growing elderly populations are the leading drivers fueling consistent adoption of anastomosis devices globally.

- Market expansion faces hurdles due to high device costs, complication risks, and stringent regulatory approvals limiting wider acceptance and surgeon adoption.

- Emerging economies and innovative technologies, particularly bioabsorbable devices, present strong growth opportunities supported by collaborations enhancing accessibility worldwide.

- Minimally invasive techniques, customized device solutions, and integration of 3D printing signify transformative trends aligning with safety, precision, and infection control priorities.

- North America led with 42.6% market share in 2023, supported by robust infrastructure, strong innovation ecosystem, and favorable reimbursement policies boosting adoption.

Regional Analysis

North America accounted for the largest share of the global anastomosis devices market in 2023, representing over 42.6% of total revenues. This share equates to a market value of approximately USD 1.7 billion. The region’s dominance is supported by the presence of advanced healthcare infrastructure and highly developed hospital networks. These systems allow widespread access to cutting-edge surgical devices, including anastomosis instruments, thereby encouraging rapid adoption. Strong institutional frameworks have made the region a leading contributor to overall industry growth.

A rising burden of chronic health conditions further strengthens market expansion in North America. Increasing rates of obesity, gastrointestinal disorders, and cardiovascular diseases create higher demand for surgeries involving anastomoses. This drives greater usage of advanced specialty instruments designed to join organs or structures. As these diseases remain prevalent across the population, the volume of procedures continues to rise. Consequently, the region experiences sustained demand for anastomosis devices, reflecting strong underlying healthcare needs.

Supportive reimbursement policies also contribute significantly to North America’s leadership position. Favorable coverage offered by both public and private payers has improved patient access to advanced surgical interventions. Minimally invasive procedures involving anastomosis are strongly encouraged through these reimbursement frameworks. This reduces cost-related barriers and enables higher adoption of innovative devices. The combined effect of economic support and efficient healthcare infrastructure creates an enabling environment for steady usage of advanced surgical instruments across hospitals and ambulatory centers.

The presence of key medtech innovators headquartered in North America further reinforces its dominance. Leading players consistently introduce improved anastomosis devices equipped with advanced technologies. These innovations focus on enhancing precision, speed, and ease-of-use during surgical procedures. The availability of such advanced instruments sustains high adoption rates within the region. Continuous product launches, coupled with early access to novel solutions, ensure that North America remains at the forefront of global market developments. This positioning is expected to remain strong over the forecast period.

Segmentation Analysis

In 2023, the Anastomosis Devices Market was largely dominated by disposable devices, which captured over 86.4% of the product share. Their strong presence was attributed to convenience, hygiene, and one-time use, which reduces infection risks and ensures sterile procedures. Healthcare professionals preferred disposable devices due to their simplicity and efficiency. In contrast, reusable devices held a much smaller portion of the market, as the industry leaned toward safer and more practical alternatives. This preference highlighted a growing focus on patient safety and clinical efficiency.

Cardiovascular surgery accounted for the largest application segment, securing 52% of the Anastomosis Devices Market in 2023. These devices proved vital in heart and vascular procedures, strengthening their clinical importance. Gastrointestinal surgery followed closely, contributing significantly to the overall market expansion. Other medical applications also showed rising adoption, underscoring the versatility of these devices. This broader usage highlighted their adaptability across multiple healthcare domains. The market’s multifaceted applications reinforced the crucial role of anastomosis devices in advancing diverse surgical procedures.

Hospitals represented the leading end-use category, with more than 58.6% share in 2023, as they manage high patient volumes and complex surgeries. Ambulatory care centers followed, with notable adoption in outpatient services. Clinics also contributed, though their share remained lower than hospitals and centers. The strong preference for hospitals reflected their comprehensive services and reliance on advanced surgical tools. This distribution revealed a clear trend toward large healthcare facilities as primary adopters, supporting the overall market’s growth and highlighting the devices’ role in modern healthcare delivery.

Key Players Analysis

The Anastomosis Devices Market is shaped by leading players such as Medtronic, LivaNova PLC, MAQUET Holding B.V. & Co. KG., and Dextera Surgical Inc. These companies drive innovation and global outreach, ensuring steady growth in the sector. Rising demand for advanced surgical solutions positions them at the forefront, setting benchmarks for performance and technology. Their collective focus on product quality, clinical needs, and patient safety strengthens market competitiveness. This dynamic presence creates a consistent flow of innovation and supports the evolution of surgical practices worldwide.

LivaNova PLC has emerged as a notable participant in the market, leveraging its expertise in cardiovascular and neuromodulation technology. The company’s anastomosis devices are recognized for precision and reliability. Strategic initiatives centered on addressing changing clinical demands strengthen its market role. LivaNova’s innovative approach and ability to align products with evolving surgical requirements ensure long-term relevance. By prioritizing patient outcomes and operational efficiency, the company contributes significantly to market growth and enhances competition among global leaders.

MAQUET Holding B.V. & Co. KG. and Dextera Surgical Inc. bring distinct advantages to the market. MAQUET focuses on precision-driven devices with a global distribution network, ensuring widespread adoption of its solutions. Its commitment to efficiency and patient outcomes enhances its market influence. Conversely, Dextera Surgical specializes in minimally invasive devices, supporting faster recovery and improved surgical performance. With its niche expertise and innovative focus, Dextera strengthens competitiveness. Together, these companies add diversity, foster innovation, and address specialized clinical needs in the anastomosis devices market.

FAQ

1. What are anastomosis devices?

Anastomosis devices are specialized medical tools used to connect two tubular structures inside the body, such as blood vessels or intestines, during surgery. They are designed to replace or assist traditional hand-sewn sutures. The devices help surgeons achieve secure and reliable connections more quickly and with greater precision. Their use reduces complications such as leakage or infections. Anastomosis devices are widely applied in complex surgical procedures where consistency and speed are vital for improving patient outcomes.

2. What are the main types of anastomosis devices?

There are several types of anastomosis devices that surgeons use depending on the procedure. Staplers are the most common and can be manual or powered. Suture-based devices are also used for precision connections. Clip-based devices provide a quick option in some surgeries, while compression devices ensure safe closures by applying uniform pressure. Recently, bioresorbable and automated devices have been developed. Each type of device has specific advantages, and the choice depends on the surgery type, patient condition, and surgeon preference.

3. In which surgeries are anastomosis devices most commonly used?

Anastomosis devices are used across several surgical specialties. They are common in cardiovascular surgeries like coronary artery bypass grafting. In gastrointestinal surgeries, such as colorectal or bariatric operations, they are widely preferred. Neurosurgeons use them in delicate brain and spinal procedures, while urological surgeries may also involve these devices. Additionally, organ transplant operations often rely on them for safe vascular or intestinal connections. Their versatility and reliability make them essential in many critical surgeries, reducing complications and improving recovery rates.

4. What are the benefits of using anastomosis devices over traditional sutures?

Anastomosis devices offer many benefits compared to traditional suturing. They save valuable time in the operating room, as procedures are completed faster. These devices also deliver consistent outcomes, reducing the risk of leaks or errors associated with manual stitching. Patients benefit from shorter hospital stays and faster recovery, which improves overall satisfaction. For surgeons, the devices simplify complex procedures, making them less labor-intensive. These advantages explain their growing adoption in modern surgeries where precision, safety, and efficiency are top priorities.

5. What are the risks or limitations of anastomosis devices?

While effective, anastomosis devices do have limitations. The biggest challenge is their high cost, which makes them less accessible in low-income regions. Device malfunctions, though rare, can create complications during surgery. In certain complex cases, irregular anatomy may also make device use difficult, forcing surgeons to revert to manual suturing. Additionally, not all hospitals have equal access to the latest devices. Despite these challenges, the devices remain valuable due to their proven ability to reduce risks in most surgeries.

6. What is driving the growth of the anastomosis devices market?

The market for anastomosis devices is growing due to several factors. Rising cases of cardiovascular and gastrointestinal diseases have increased surgical needs worldwide. The demand for minimally invasive surgeries is also boosting adoption, as devices improve precision and outcomes. Growing geriatric populations require more surgical care, further fueling demand. In addition, continuous advancements in medical technology are making these devices safer and more effective. Together, these drivers are creating steady growth opportunities for manufacturers and healthcare providers across regions.

7. What is the current size of the anastomosis devices market?

The global anastomosis devices market is valued at around USD 4.1 billion as of 2023. It is expected to expand steadily over the coming years at a compound annual growth rate (CAGR) of 6.1 percent. This growth is supported by rising surgical volumes and wider adoption of advanced devices. Both developed and emerging markets are contributing to expansion. While North America holds the largest share, Asia-Pacific is projected to see the fastest growth due to healthcare investments.

8. Which regions dominate the market?

Currently, North America dominates the global anastomosis devices market. This is due to advanced healthcare infrastructure, high surgical volumes, and strong adoption of innovative technologies. Europe follows with widespread use of minimally invasive procedures. The Asia-Pacific region, however, is emerging as the fastest-growing market. Increasing healthcare investments, growing patient numbers, and rising medical tourism are driving its growth. Other regions such as Latin America and the Middle East are also showing gradual adoption. Regional growth depends on accessibility and affordability.

9. Who are the key players in the market?

Several global companies lead the anastomosis devices market. Key players include Medtronic plc, Johnson & Johnson (Ethicon), Intuitive Surgical, B. Braun Melsungen AG, and Baxter International. Synovis Micro Companies Alliance is also a recognized participant. These companies are known for innovation, strong product portfolios, and global reach. They invest in research and development to introduce advanced devices with better safety and efficiency. Competition in the market remains intense, with firms focusing on partnerships, acquisitions, and new product launches to expand.

10. What challenges does the market face?

The anastomosis devices market faces several challenges despite strong growth. High device costs continue to limit adoption, especially in developing economies. Strict regulatory approval processes also delay new product launches. In addition, limited awareness and training among surgeons in some regions slow adoption rates. Competition from traditional manual suturing remains in low-resource hospitals where affordability is a concern. These challenges require manufacturers to balance innovation with affordability. Overcoming these barriers will be critical for sustained and widespread market expansion.

11. What are the emerging trends in the market?

Several new trends are shaping the future of the anastomosis devices market. Robot-assisted surgeries are increasing, creating demand for compatible devices. There is also a growing shift toward bioabsorbable materials, which reduce complications and improve healing. Automated solutions are being developed to minimize errors and enhance surgical efficiency. The focus on minimally invasive procedures continues to drive innovation. In addition, increasing research and development efforts are aimed at making devices more affordable and adaptable. These trends point to strong future growth.

Conclusion

The anastomosis devices market is set for strong and steady growth, supported by rising surgical procedures, technological advances, and the growing elderly population. Demand is being shaped by the increasing adoption of minimally invasive and robotic-assisted surgeries, as these devices provide faster recovery, reduced complications, and improved efficiency compared to traditional methods. Disposable devices dominate due to their safety and convenience, while hospitals remain the primary end users. Despite challenges such as high costs and strict regulations, opportunities in emerging economies and the introduction of bioabsorbable solutions continue to create room for expansion. With ongoing innovation and strategic partnerships, the market is expected to remain highly competitive and dynamic.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)