Table of Contents

Overview

The Global Amniotic Products Market is projected to reach USD 2.4 billion by 2033. Growth has been driven by the rising use of regenerative therapies across clinical settings. Amniotic membranes and fluids have been adopted due to their natural healing support and anti-inflammatory benefits. Their ability to reduce scarring has increased acceptance among physicians seeking minimally invasive and biologically based solutions. As hospitals prioritize therapies that improve recovery outcomes, demand for these products has strengthened across major care segments.

The prevalence of chronic wounds, diabetic ulcers, and orthopedic injuries has been increasing. These conditions require effective and advanced healing materials. Amniotic products have been used in wound care, sports medicine, and musculoskeletal treatments because they support faster tissue repair. The rise in aging populations has further contributed to higher treatment volumes. The expanding patient base has played a key role in sustaining market growth, as clinicians prefer solutions with consistent clinical performance.

Surgical applications have widened across ophthalmology, dermatology, and reconstructive procedures. Amniotic grafts are valued for their ability to protect tissues and support regeneration during and after surgery. Their use in eye care, skin grafting, and cosmetic procedures has intensified as global surgical volumes increase. This diversification across medical specialties has created steady adoption and placed amniotic materials as a dependable option for complex and routine procedures.

Clinical research has reinforced confidence in the safety and efficacy of amniotic tissues. Ongoing studies have helped broaden physician awareness and improve acceptance among healthcare providers. Technological advancements in processing have also improved product quality. Enhanced preservation and sterilization methods allow manufacturers to maintain the biological integrity of tissues while improving shelf life. These innovations have supported broader product availability and strengthened supplier capability across regions.

Supportive healthcare trends and better reimbursement in some markets have aided adoption. Hospitals continue to favor treatments that shorten recovery time and reduce long-term complications. Growing distribution networks and stronger market awareness have further facilitated access. As partnerships expand, more clinics integrate amniotic products into treatment protocols. These combined factors have established a stable growth path for the market and created sustained opportunities over the forecast period.

Key Takeaways

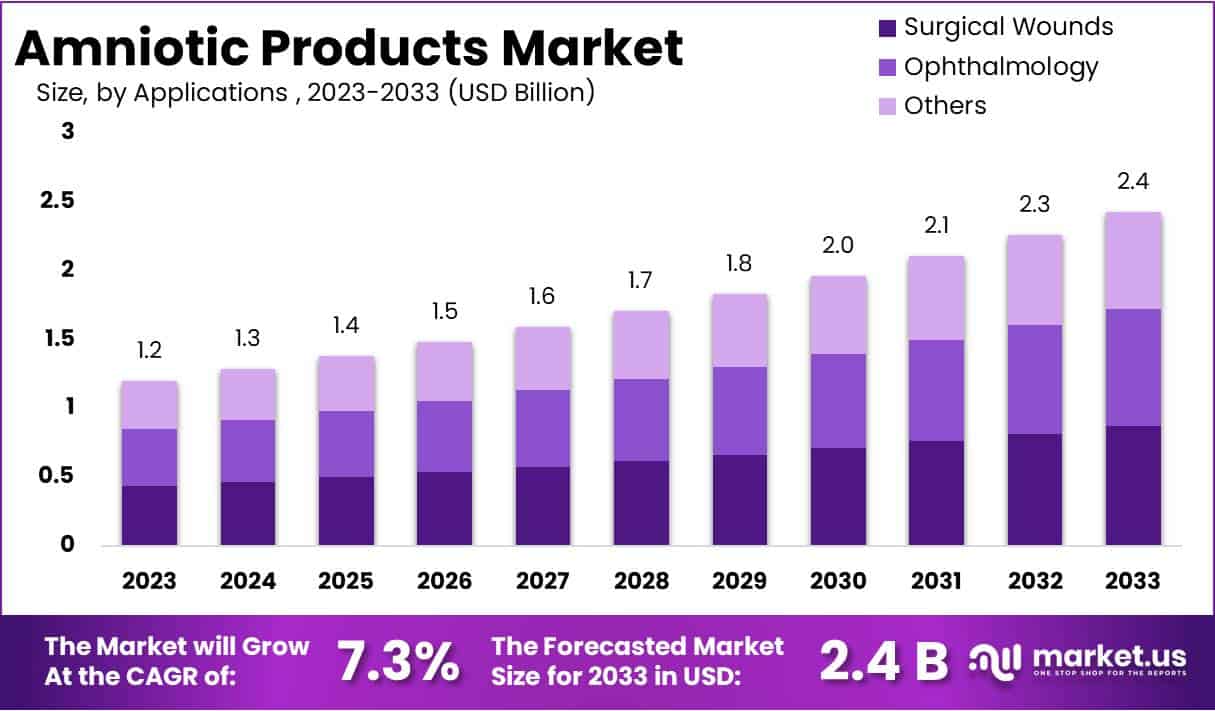

- The market was projected to rise from USD 1.2 billion in 2023 to USD 2.4 billion by 2033, supported by a sustained CAGR of 7.3%.

- Cryopreserved amniotic membrane was reported to command over 52% share in 2023, driven by strong clinical effectiveness and extended shelf-life advantages.

- Surgical wound management was identified as the largest application, holding more than 36% share due to consistent demand for products that improve healing outcomes.

- Hospitals were observed to be the primary end-use facilities, representing over 41% share through broad adoption of amniotic products across diverse clinical procedures.

- Growth opportunities were highlighted in regenerative medicine, where natural healing characteristics of amniotic products continued to increase adoption potential.

- Orthopedics and sports medicine were noted for rising usage, supported by evidence of reduced inflammation and accelerated tissue recovery.

- North America was recognized as the leading regional market with 34% share, strengthened by advanced healthcare systems and substantial research and development activities.

Regional Analysis

In 2023, North America held a leading position in the amniotic products market with a share exceeding 34% and a market value of USD 0.4 billion. The region’s dominance was supported by a strong healthcare system that enabled the use of advanced medical technologies. Hospitals and specialized clinics ensured effective distribution and utilization of these products. This structure created steady demand across key therapeutic areas. Overall, the established medical environment supported the growth of amniotic products throughout the region.

Advanced R&D activities strengthened North America’s position in the global market. Biotech and pharmaceutical companies invested in developing new formulations and applications. These investments resulted in continuous product improvements. The advancements increased the clinical value of amniotic products in wound care, orthopedics, and ophthalmology. Research institutions also contributed by supporting trials and generating evidence. This environment ensured a stable pipeline of innovative solutions. As a result, technological leadership became a major driver of market expansion within the region.

Growing awareness among healthcare professionals and patients supported wider adoption of amniotic products. The recognized benefits, including enhanced wound healing and reduced inflammation, increased their use in clinical practice. Training programs, workshops, and educational campaigns improved understanding of product advantages. Positive patient outcomes strengthened trust and acceptance. These factors encouraged higher procedure volumes across medical specialties. As awareness continued to rise, demand for regenerative therapies expanded, reinforcing the market’s upward trajectory across North America.

A strong regulatory system further supported the regional market. Agencies such as the FDA and Health Canada established guidelines that ensured product safety and efficacy. This framework encouraged responsible innovation and reduced market risks. Companies operated within clear standards, which improved product quality and patient confidence. As the focus on regenerative medicine increased, supportive regulations played a key role in market development. With ongoing advancements and a commitment to high clinical standards, North America is expected to maintain its influence in the global amniotic products market.

Segmentation Analysis

The Cryopreserved Amniotic Membrane segment maintained a leading market position in 2023. It accounted for more than a 52% share of the amniotic products market. Its dominance was supported by wide adoption in ophthalmology, wound care, and surgical procedures. Higher efficacy and long shelf life strengthened its preference among clinicians. Advancements in preservation methods enhanced biological activity and usability. Strong clinical evidence further validated its healing and anti-inflammatory benefits. The Lyophilized Amniotic Membrane segment also expanded due to lower costs and simple storage needs.

The Surgical Wounds segment held a dominant position in 2023, capturing over a 36% share of the applications market. The rising need for advanced healing solutions supported its growth. Amniotic products reduced inflammation and scarring in surgical sites. They also helped improve recovery outcomes. The Ophthalmology segment recorded strong engagement due to increasing use in corneal disorders and dry eye treatment. Aging populations and rising eye disease prevalence reinforced demand. Other areas, including orthopedics and chronic wounds, continued to adopt amniotic products for improved healing performance.

Hospitals accounted for more than a 41% share of the end-user segment in 2023, reflecting extensive use across therapeutic and surgical care. High patient volume and broad service offerings reinforced their leading role. Ambulatory surgical centers followed with notable adoption, driven by growth in outpatient procedures. Specialized clinics also contributed significantly by using amniotic products in targeted treatments. Research centers and laboratories formed a smaller but essential segment. Their work supported innovation, testing, and development of new applications within the amniotic products market.

Key Market Segments

By Product

- Cryopreserved Amniotic Membrane

- Lyophilization Amniotic Membrane

By Applications

- Surgical Wounds

- Ophthalmology

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialized Clinics

- Research Centers & Laboratory

Key Players Analysis

The amniotic products market is shaped by companies that focus on innovation in regenerative medicine and advanced biologics. Their technologies support wound healing, tissue repair, and surgical recovery. Strong research programs and quality standards guide product development across applications in orthopedics, wound care, and surgical procedures. Allosure Inc., Amnio Technology LLC, and Applied Biologics LLC demonstrate strong capabilities through continuous innovation and adherence to safety and efficacy requirements.

The market is strengthened by organizations that invest in advanced processing methods and clinical validation. Their efforts ensure reliable allografts and surgical biomaterials for healthcare providers. Companies such as FzioMed Inc., Human Regenerative Technologies LLC, and Integra Lifesciences Holdings Corporation contribute to improved patient outcomes. Their products are designed to reduce complications, promote healing, and expand clinical acceptance in multiple medical fields.

Strategic collaborations, distribution networks, and regulatory compliance are central to sustaining competitiveness. Firms actively expand their presence through partnerships with hospitals, clinics, and surgical centers. Corza Ophthalmology, MiMedx Group Inc., and Skye Biologics Inc. emphasize strong commercialization strategies. Their investment in quality control and product reliability enhances customer trust and supports long-term market penetration.

Ongoing research and product diversification continue to drive market growth. Companies work to refine processing technologies, improve graft consistency, and address unmet clinical needs. Tissue-Tech Inc. and other key players support broader adoption of amniotic-based therapies across specialties. Their focus on performance, safety, and scientific evidence contributes to sustained demand. This collective commitment strengthens the competitive landscape and shapes future developments in the amniotic products market.

Market Key Players

- Allosure Inc.

- Amnio Technology LLC

- Applied Biologics LLC

- FzioMed Inc.

- Human Regenerative Technologies LLC

- Integra Lifesciences Holdings Corporation

- Corza Ophthalmology

- MiMedx Group Inc.

- Skye Biologics Inc.

- Tissue-Tech Inc.

Challenges

1. Limited Clinical Evidence

The adoption of amniotic products remains slow because long-term clinical evidence is limited. Healthcare providers usually require strong, peer-reviewed data before introducing new therapies into advanced care pathways. The absence of robust studies has created hesitation among clinicians and decision-makers. As a result, the market faces barriers in gaining broad acceptance, especially in settings where safety, proven efficacy, and long-term outcomes are essential for treatment approval and routine clinical use.

2. Variations in Regulatory Requirements

Regulatory requirements differ widely across countries, and this variation has slowed market expansion. Each region follows its own approval pathway, documentation standards, and compliance rules. These differences cause delays in product launches and increase regulatory costs for manufacturers. Companies must invest additional time and resources to meet country-specific obligations. This environment has created operational inefficiencies, limited speed-to-market, and raised financial burdens for firms working to introduce amniotic products globally.

3. High Cost of Processing and Storage

The processing of amniotic membranes and fluids requires advanced equipment and specialized laboratory procedures. These activities involve strict quality controls and temperature-regulated storage systems. As a result, production costs remain high, and final product prices increase. This has created financial pressure for healthcare facilities, especially smaller clinics with limited budgets. The high cost structure reduces adoption rates and restricts broader access to amniotic products in both developed and emerging healthcare markets.

4. Supply Dependence on Donor Availability

The supply of amniotic materials depends entirely on voluntary donations. Any decline in donor participation immediately affects the availability of raw biological materials. This dependence creates uncertainty in production planning and limits stable inventory levels. Manufacturers often face fluctuations in supply, which can disrupt distribution channels. This instability reduces the market’s ability to meet rising demand and restricts long-term growth opportunities across different therapeutic segments.

5. Lack of Standardized Product Quality

Standardized quality benchmarks for amniotic products are still evolving. Manufacturers use different processing techniques, preservation methods, and validation protocols. These variations create inconsistencies in product performance, safety, and clinical outcomes. Healthcare providers often raise concerns when quality varies between brands. This lack of uniform standards slows adoption and reduces trust among clinicians. Establishing clear guidelines and harmonized specifications is essential to improve market confidence and ensure reliable therapeutic results.

6. Limited Awareness Among Clinicians

Awareness of amniotic product benefits remains limited among many clinicians. Training programs and educational initiatives are still insufficient in several regions. As a result, healthcare professionals may not fully understand the therapeutic applications or the clinical value offered by these products. This knowledge gap restricts their use in hospitals, specialty clinics, and outpatient settings. Improved clinician education is required to increase adoption and support wider integration into routine treatment practices.

Opportunities

1. Rising Preference for Natural and Regenerative Therapies

The market has shown strong interest in natural and regenerative therapies. This demand is growing in wound care, orthopedics, and ophthalmology. Amniotic products fit well with this shift because they support healing and reduce complications. Their natural origin is gaining trust among clinicians and patients. As healthcare systems move toward safer and more biological treatment options, the use of amniotic-based solutions is expected to rise steadily.

2. Expanding Use in Chronic Wound Management

Chronic wounds remain a major global concern, with diabetic foot ulcers, burns, and pressure injuries increasing every year. Amniotic products have shown strong healing potential in these cases. Their ability to reduce inflammation and support tissue repair has created wider clinical acceptance. Hospitals and clinics are using these products more often because they help improve outcomes. This trend is expected to continue as demand for effective chronic wound treatments grows.

3. Technological Advancements in Processing

New processing techniques have improved the safety and performance of amniotic products. Better sterilization methods and enhanced preservation systems have strengthened product reliability. These advancements have also increased shelf life, which supports wider distribution. Manufacturers can now maintain higher quality standards because of improved technology. As the technology continues to evolve, more innovative products are expected to enter the market. This progress is helping companies meet rising clinical expectations.

4. Growth in Outpatient and Ambulatory Care Settings

Healthcare delivery has shifted toward outpatient and ambulatory care because these settings lower costs and reduce hospital stays. Amniotic products support this shift due to their simple application and lower procedure complexity. They can be used quickly in clinics without advanced equipment. This makes them suitable for busy care environments. As outpatient centers continue to expand, demand for easy-to-use wound-healing materials is expected to grow. This trend supports broader market adoption.

5. Strategic Partnerships and Collaborations

Partnerships between biotech firms, tissue banks, and healthcare providers have increased across the sector. These collaborations help companies expand research and strengthen product pipelines. Shared resources and expertise also improve product quality and speed up development. Distribution networks become stronger through joint efforts. As collaboration grows, more advanced solutions are expected to reach the market. These alliances are shaping future innovation and supporting long-term market growth.

6. Increasing Investment in Regenerative Medicine

Investment in regenerative medicine has grown steadily as interest in biological treatments increases. Funding from private and public sources supports new product development and clinical research. This investment accelerates innovation and improves scientific understanding. As research expands, amniotic products gain more visibility and credibility. Greater investment also encourages companies to explore new applications. This growth is expected to support broader clinical adoption in the coming years.

Conclusion

The amniotic products market is expected to maintain steady growth as demand for natural healing solutions strengthens across medical fields. Increased use in wound care, orthopedics, and surgical procedures has supported broader acceptance among clinicians. Advancements in processing have improved product quality, while growing awareness has encouraged wider clinical adoption. Although challenges such as varying regulations and high production costs remain, rising interest in regenerative therapies continues to create new opportunities. Ongoing research, improved distribution networks, and supportive healthcare trends are expected to reinforce market expansion. Overall, amniotic products are positioned as reliable options for enhancing healing and improving patient outcomes in diverse care settings.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)