Table of Contents

Overview

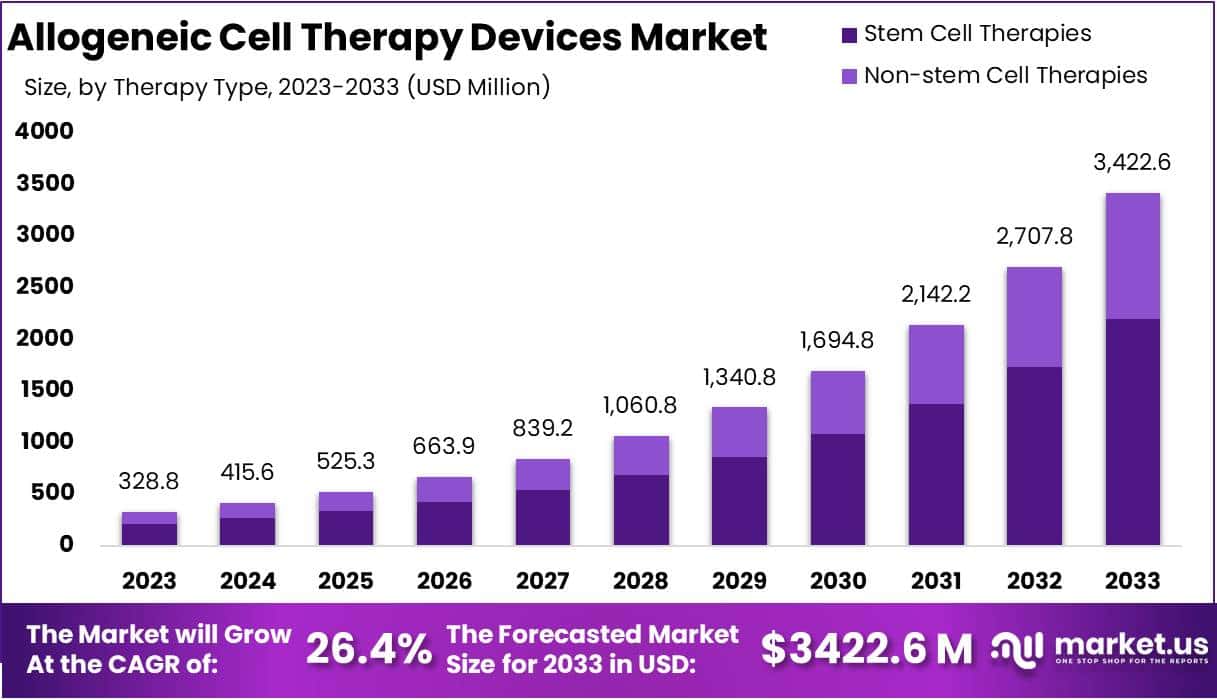

The Global Allogeneic Cell Therapy Devices Market is projected to reach USD 3,422.6 million by 2033, rising from USD 328.8 million in 2023 at a CAGR of 26.4%. Growth is being supported by rising demand for off-the-shelf therapies, expanding clinical pipelines, and stronger regulatory clarity. Allogeneic products allow one donor to treat multiple patients, which reduces production time and increases scalability. This model requires advanced bioreactors, automated cell-processing systems, and reliable quality control tools. As hospitals and CDMOs scale capacity, investments in standardized, closed, and automated devices continue to rise.

The therapeutic landscape is broadening beyond hematologic cancers to include neurological, autoimmune, and inflammatory diseases. Late-stage programs involving NK cells, MSCs, and engineered T-cell products are expanding clinical-grade manufacturing requirements. This trend increases demand for devices used in large-scale expansion, product formulation, cryopreservation, and controlled thawing. Approvals of off-the-shelf cell therapies have validated commercial potential and encouraged developers to adopt technologies that support consistent batch production and long-term storage stability.

Scalable and cost-efficient manufacturing has become essential for commercial adoption. Traditional planar systems are no longer adequate for high-volume production. Industry efforts are focusing on stirred-tank and perfusion bioreactors, microcarrier technologies, and automated processing platforms. These systems support closed, continuous, or semi-continuous culture and enable real-time monitoring of viability, density, and nutrient levels. Their adoption is driving higher yields, lower costs, and improved reproducibility, which strengthens their role in allogeneic manufacturing workflows.

Technological innovation is reshaping device design across the value chain. Single-use bioreactors, integrated sensors, modular downstream systems, and automated fill-finish platforms are improving process control and regulatory alignment. At the same time, new FDA guidance on allogeneic cell safety and manufacturing comparability has elevated expectations for contamination control and documentation. As a result, developers are moving toward automated, enclosed, and GMP-compliant systems to reduce operator-dependent risk and ensure consistent product quality.

Overall, the market is expanding due to increasing investment, facility build-outs, and digital transformation. Pharmaceutical companies and CDMOs are strengthening allogeneic capabilities through partnerships and infrastructure upgrades. Improved cryopreservation, monitored storage, and standardized thawing systems support reliable distribution across treatment centers. Meanwhile, digital tools and in-line analytics enhance batch monitoring and quality control for larger therapeutic volumes. Together, these factors reinforce sustained demand for advanced devices that support efficient, safe, and scalable delivery of allogeneic cell therapies.

Key Takeaways

- The Allogeneic Cell Therapy Devices market recorded USD 328.8 million in revenue and is expected to reach USD 3422.6 million, driven by a 26.4% CAGR.

- The stem cell therapy segment dominated revenue generation, securing a 64.2% market share and establishing itself as the primary contributor within the overall industry landscape.

- The hematological disorders category led therapeutic areas in 2023, capturing a 43.8% share and demonstrating its strong clinical adoption across diverse patient populations.

- Hospitals and clinics served as the principal end-users in 2023, reflecting sustained utilization of allogeneic cell therapy devices across established care settings.

- North America maintained its leading regional position, achieving a 39.2% revenue share and demonstrating strong infrastructure support for advanced allogeneic cell therapy adoption.

Regional Analysis

North America is leading the allogeneic cell therapy devices market due to its strong healthcare structure. The region has advanced hospitals, research centers, and medical universities. These institutions support the development and use of innovative cell therapy devices. A clear regulatory system further strengthens the market. Approvals and guidelines are well-defined. This creates confidence among investors and manufacturers. As a result, product commercialization becomes easier. These factors have supported the region’s dominant revenue share and have reinforced its favorable position in the global market.

The region’s regulatory clarity has played a major role in market expansion. Strict but transparent rules help companies plan development and launch timelines. Research collaboration between academic institutes and industry partners is also strong. Investment in innovation remains steady. This supports early-stage trials and device advancements. Healthcare providers in North America adopt new technologies faster. This drives market penetration. Such conditions create a stable environment for continued growth. These structural strengths ensure that North America maintains leadership in the allogeneic cell therapy devices market.

The Asia-Pacific region is expected to record the highest CAGR during the forecast period. The growth is supported by major investments in healthcare infrastructure. Countries such as China, Japan, South Korea, and India are expanding specialized centers for cell-based therapies. Healthcare spending is rising across the region. Chronic disease cases are increasing as well. Awareness of advanced treatment solutions is also growing. These factors increase demand for allogeneic cell therapy devices. As a result, the region is becoming a key growth hub for global market participants.

Segmentation Analysis

The stem cell therapy segment held a revenue share of 64.2% in 2023. Its dominance can be attributed to its strong therapeutic potential and its wide use in treating leukemia, lymphoma, blood cancers, and several autoimmune disorders. Stem cells offer the ability to differentiate into multiple cell types, which increases their clinical value. Non-stem cell therapies are projected to grow steadily. These therapies rely on differentiated or immune cells, including T-cell therapies, dendritic cell therapies, islet cell transplantation, and chondrocyte-based treatments.

The hematological disorders segment accounted for 43.8% of the market share in 2023. This position is supported by the rising global incidence of leukemia, lymphoma, and related conditions. These disorders have long been treated with allogeneic procedures such as hematopoietic stem cell transplantation. This method replaces diseased blood cells with healthy donor cells. Dermatological disorders are expected to grow at the fastest pace. Their expansion is driven by increasing awareness of allogeneic stem cell-based treatments for wound healing, skin aging, scar repair, and autoimmune skin diseases.

Hospitals and clinics represented the leading end-user group with a 43.7% revenue share. Their dominance is linked to their central role in administering cell therapies and managing patient care. These facilities serve as primary treatment centers for individuals receiving allogeneic cell-based interventions. Research institutes, academic centers, and biotechnology companies also support market development through innovation and clinical studies. However, hospitals and clinics continue to drive the highest adoption of allogeneic cell therapy devices due to direct patient engagement and established care infrastructure.

Key Market Segments

By Therapy Type

- Stem Cell Therapies

- Non-stem Cell Therapies

By Therapeutic Area

- Hematological Disorders

- Dermatological Disorders

- Others

By End-User

- Hospitals & Clinics

- Research & Academic Institutes

- Biotechnology & Pharmaceutical Companies

- Others

Key Players Analysis

The competitive landscape of the allogeneic cell therapy devices market has been shaped by continuous innovation and expanding clinical applications. Strong emphasis has been placed on advancing cell-based technologies to improve therapeutic outcomes. Major companies have increased their investments to enhance manufacturing efficiency and scalability. This approach has supported the development of next-generation allogeneic platforms. Firms such as Novartis AG and Gilead Sciences, Inc. have been at the forefront, driving technological progress and strengthening their capabilities through focused R&D programs and strategic expansion initiatives.

Market growth has been supported by active participation from companies aiming to broaden their portfolios and reinforce global presence. Collaborative agreements have been widely used to accelerate product development and access emerging opportunities. Regulatory advancements have created favorable conditions for innovation, prompting additional investments across the industry. Leading organizations, including Celgene Corporation, Bluebird Bio, Inc., and Pfizer Inc., have adopted structured strategies to enhance market penetration, optimize production processes, and advance novel allogeneic therapies.

Competitive positioning has been influenced by mergers, acquisitions, and strategic partnerships designed to increase operational strength. Technology upgrades have contributed to improved device performance and reliability, supporting wider adoption in clinical settings. Companies have focused on scaling manufacturing systems to meet rising demand for standardized therapies. Organizations such as Allogene Therapeutics and other emerging players have expanded their research pipelines and strengthened distribution capabilities, contributing to a dynamic and evolving market environment that continues to attract sustained investment and development activities.

Challenges

1. Complex Manufacturing Processes

The manufacturing of allogeneic cell therapy devices involves highly controlled conditions. Each step requires specialized tools, cleanroom environments, and strict monitoring. Even small variations in temperature, handling, or timing can affect the stability and quality of the final product. This sensitivity increases operational difficulty for producers and reduces process flexibility. The need for advanced technologies also adds financial pressure. High-precision equipment, automated systems, and skilled technical teams must be in place to maintain consistency. As a result, overall production costs rise, and manufacturers face challenges in scaling their operations efficiently while keeping quality intact.

2. Strict Regulatory Requirements

The market is shaped by strict rules set by regulatory bodies. Each device must meet detailed safety, quality, and performance criteria. Approval processes are long and require multiple rounds of documentation, testing, and inspection. This extends timelines for product launches and increases the workload for compliance teams. Companies must invest heavily in regulatory expertise and audit preparation. Any delay in meeting requirements can slow market entry and affect competitiveness. These regulations are designed to protect patient safety, but they add significant cost and complexity for manufacturers operating in the allogeneic cell therapy device segment.

3. High Risk of Contamination

Allogeneic cell therapies rely on donor-derived cells, which raises the risk of contamination during collection, processing, and storage. Maintaining sterility is crucial at every stage, and even a minor lapse can compromise the therapy. Devices used in handling must ensure airtight conditions and support strict aseptic practices. Advanced monitoring systems are also required to detect contamination early. This increases operational pressure on manufacturers and laboratory teams. The risk becomes higher when multiple batches are processed simultaneously. To manage these challenges, companies must invest in rigorous quality-control frameworks, specialized facilities, and highly trained personnel.

4. Limited Standardization

The industry currently lacks well-defined global standards for cell handling, storage, and delivery devices. Different regions follow varying guidelines, which leads to inconsistencies in product design, performance, and safety. Manufacturers must adjust their devices to meet local requirements, increasing development time and cost. Limited standardization also affects interoperability, as devices may not align with other systems used in clinical or manufacturing settings. This variability slows innovation and creates uncertainty for producers. Achieving consistent quality becomes difficult when each market operates under its own rules. Standardized frameworks would support smoother adoption and stronger product reliability.

5. High Initial Investment

Developing allogeneic cell therapy devices requires a significant financial commitment. Companies must invest in specialized facilities, advanced equipment, and highly skilled personnel. Cleanrooms, automation systems, and high-grade materials add to the overall cost. These requirements create barriers for new entrants and limit the number of players in the market. Established companies must also allocate budget for continuous upgrades, as the technology evolves rapidly. The high initial investment affects profitability, especially in the early stages of commercialization. As a result, manufacturers must plan long-term strategies to ensure sustainable returns in this capital-intensive environment.

6. Supply Chain Constraints

The supply chain for allogeneic cell therapy devices is highly sensitive and depends on reliable donor cell sourcing and temperature-controlled logistics. Any disruption can affect product integrity and lead to therapy failure. Transportation must support consistent cold-chain conditions, and delays can compromise cell viability. Limited availability of suitable donors adds another challenge. Manufacturers must coordinate with multiple partners, including logistics providers and donor banks, to maintain supply stability. These dependencies make scaling production more difficult. Building resilient supply networks, supported by advanced tracking systems, is essential for long-term growth and market reliability.

Opportunities

1. Growing Focus on Off-the-Shelf Therapies

The demand for off-the-shelf allogeneic therapies is rising because these products can be produced in advance and used when needed. This model reduces the long waiting times linked with autologous therapies. It also supports better scalability, as one batch can serve many patients. As a result, devices that enable mass production, standardized workflows, and consistent output are expected to gain traction. Manufacturers that offer reliable equipment for large-volume processing are likely to benefit from this shift. The market growth is supported by the broader trend toward faster delivery and more accessible treatment options.

2. Advancements in Bioprocessing Technologies

New bioprocessing technologies are transforming the efficiency of allogeneic cell therapy production. Automated cell expansion systems, closed-system processing tools, and modern cryopreservation devices now allow safer and more stable workflows. These technologies reduce contamination risks and help maintain cell quality at scale. As efficiency improves, the need for next-generation devices grows stronger. Manufacturers can introduce innovative solutions that support continuous production and predictable output. The adoption of these technologies improves cost control while supporting consistent performance. The shift toward advanced bioprocessing is expected to create steady growth opportunities in the device market.

3. Expansion of Clinical Trials

Clinical trials for allogeneic therapies are increasing in areas such as oncology, immune disorders, and regenerative medicine. This expansion is boosting the demand for specialized devices required for research, testing, and early-stage manufacturing. Laboratories and research centers need equipment that supports safe cell handling, quality control, and efficient processing. As more candidates move into mid- and late-stage trials, the need for reliable and scalable devices becomes even stronger. This trend is encouraging manufacturers to design tools that meet strict regulatory and operational needs. Continued growth in clinical research is expected to support significant market opportunities.

4. Rising Investment in Cell-Based Medicine

Investment in cell-based medicine is increasing across pharmaceutical companies, biotech firms, and government organizations. These funds support new research programs and the development of innovative therapies. Such investment also drives growth in the demand for devices used in testing, manufacturing, and distribution. More capital allows companies to improve infrastructure and adopt advanced technologies. This environment supports the introduction of high-performance equipment tailored for allogeneic cell therapy. As funding expands, the market becomes more favorable for device manufacturers offering strong capabilities and reliable performance.

5. Demand for Scalable Manufacturing Platforms

The shift toward commercial-scale production is creating strong demand for scalable manufacturing platforms. Allogeneic therapies require systems that can produce large batches while maintaining consistent quality. Devices that support controlled expansion, automated monitoring, and large-volume handling are becoming essential. Manufacturers that provide scalable, modular, and flexible solutions are likely to gain a strategic advantage. As therapy pipelines move toward approval and commercialization, the need for industrial-grade equipment will continue to rise. This demand represents a major growth opportunity for companies focused on long-term production capabilities.

6. Increasing Use of Automation

Automation is becoming vital in allogeneic cell therapy manufacturing, as it reduces human error and improves consistency. Devices equipped with automated control systems, sensors, and digital analytics offer better reliability during production. These tools help maintain stable environments, ensure precise monitoring, and reduce operational risks. Automation also supports faster workflows and lower labor costs. As quality and efficiency become more important, automated devices are gaining broader acceptance across research labs and production facilities. This trend is expected to strengthen opportunities for manufacturers that provide smart and interconnected equipment.

Conclusion

The market for allogeneic cell therapy devices is advancing steadily as demand for safe, scalable, and ready-to-use treatments continues to rise. Growth is being supported by expanding clinical programs, stronger regulatory clarity, and wider adoption of automated and closed-system technologies. Progress in bioprocessing, cryopreservation, and quality control is improving efficiency and reliability across manufacturing workflows. Healthcare providers and developers are investing in modern infrastructure to support consistent production and long-term storage needs. As innovation accelerates and partnerships strengthen, the sector is expected to maintain stable momentum. The overall outlook remains positive, driven by broader therapeutic use and increasing confidence in allogeneic platforms.

View More

Stem Cell Therapy Market || CAR-T Cell Therapies Market || Autologous Cell Therapy Market || Cell Therapy Monitoring Kits Market || Personalized Cell Therapy Market || Cell Therapy Market || Automated and Closed Cell Therapy Processing Systems Market || Cell Therapy Manufacturing Market || Cell Therapy Raw Materials Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)