Table of Contents

Overview

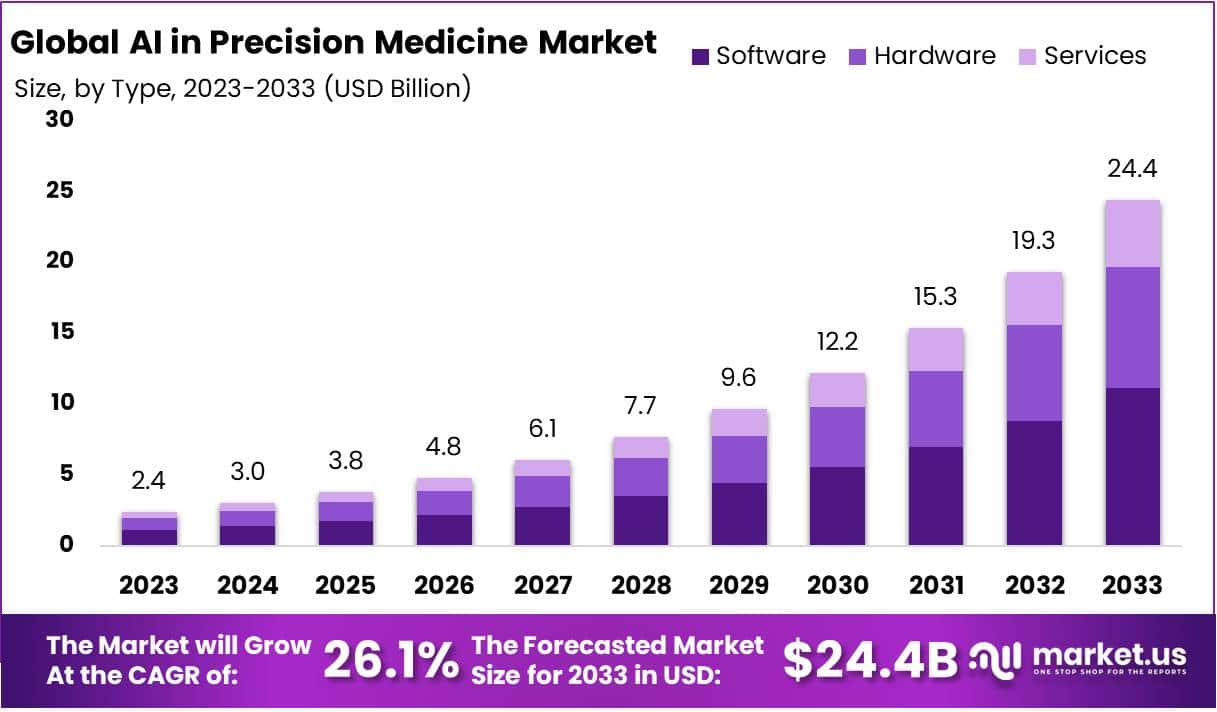

The global AI in Precision Medicine Market is projected to reach USD 24.4 Billion by 2033, increasing from USD 2.4 Billion in 2023. A CAGR of 26.1% is anticipated during 2024–2033. Market expansion is being supported by a rising need for personalized therapy and increasing digitalization in healthcare. Noncommunicable diseases remain a major global burden, with the WHO reporting over 43 million deaths in 2021. Growing cancer incidence has increased adoption of AI-driven diagnostic and treatment tools, enabling more targeted interventions.

The adoption of electronic health records has advanced significantly. An OECD survey confirmed that 27 countries have deployed mature eHR systems, while 24 maintain core datasets to improve data exchange. Patient access to digital records increased in 23 countries by 2021. This digital foundation provides larger volumes of structured clinical data for AI models. Improved interoperability and enhanced data quality standards have strengthened model training and supported clinical decision-making processes.

Genomics has become a major catalyst. DNA sequencing costs have declined consistently since 2001, as tracked by the U.S. National Human Genome Research Institute. More affordable sequencing enables wide-scale genomic profiling across diverse populations. Large public health cohorts are expanding. The NIH All of Us program has collected data from more than 633,000 participants, including biosamples, wearable data, and eHR records. This depth of data allows AI-enabled models to generate precise risk predictions and treatment recommendations at a population level.

Policy and regulatory developments have reinforced market stability. The U.S. FDA has maintained a public list of authorized AI/ML medical devices, guiding evidence standards and accelerating approvals. In Europe, the EMA has issued detailed guidance on AI across the medical lifecycle. WHO’s ethical recommendations for large multi-modal health models have strengthened safety, transparency, and fairness frameworks. Regulatory clarity has encouraged clinical adoption and investor confidence, supporting commercialization across health systems.

Public funding and cross-border collaborations are also accelerating deployment. The NHS AI Lab and AI in Health and Care Award in England are advancing real-world evaluation of AI technologies in care pathways. The European Commission’s 1+ Million Genomes initiative is enhancing secure data access and common standards across Member States. These initiatives promote interoperability, evidence generation, and scalable deployment. Continued improvements in data quality, federated sharing, and transparent validation are expected to sustain long-term growth in AI-enabled precision medicine.

Key Takeaways

- AI-enabled software solutions are demonstrating strong effectiveness in disease detection and diagnosis, driving meaningful expansion within the software segment in precision medicine.

- Deep learning technologies currently account for 36.2% of the market share, reflecting their substantial contribution to AI-driven advancements in precision healthcare.

- The oncology segment continues to adopt AI-powered platforms rapidly, showcasing AI’s expanding influence in cancer diagnosis, treatment planning, and therapeutic support.

- Growing elderly demographics, frequently impacted by chronic and complex diseases, are expected to create sustained demand for AI-based healthcare solutions that enhance patient outcomes.

- Data privacy and security concerns remain a major restraint, with potential risks in handling sensitive patient information likely to hinder accelerated adoption.

Regional Analysis

North America is expected to witness strong growth during the forecast period. The region has built a solid market position due to the presence of established companies such as Mead Johnson and Company and Abbott Laboratories. A market share of 32.4% was recorded in 2023, reflecting the region’s competitive strength. This growth has been supported by strategic collaborations among industry players. Active participation from public and private stakeholders has strengthened innovation and enhanced access to advanced healthcare solutions across the region.

The region benefits from favorable demographic and lifestyle factors. An increasing elderly population and rising cases of sedentary behavior have contributed to a higher prevalence of chronic health disorders. These dynamics support steady demand for advanced healthcare products and treatment options. Continued investment in health research and awareness initiatives has enabled the development of targeted therapies and preventive healthcare solutions. As a result, significant commercial opportunities are being created across specialized medical segments.

Digital health transformation has also accelerated growth in North America. The expansion of health-related datasets and digital diagnostic resources has strengthened the region’s research capabilities. Enhanced access to clinical information has supported the development of precision medicines and improved treatment outcomes. This has led to faster innovation cycles and the introduction of new therapies. The digital infrastructure in the region continues to attract technology-driven healthcare companies, which further boosts industry advancement and competitiveness.

Key strategic movements are shaping future market expansion. A US-based intergovernmental estimate from May 2023 indicated that chronic illnesses may cause 86% of the expected 90 million deaths by 2050. This highlights the urgent need for effective treatments. Additionally, Certara, Inc. began a two-year collaboration with Memorial Sloan Kettering Cancer Center to create a bio-simulation platform for CAR-T cell therapies. Such initiatives emphasize the region’s focus on advanced biomedical research and high-value therapeutic innovation.

Segmentation Analysis

The AI in precision medicine market has been segmented into hardware, software, and services. AI-based software solutions accounted for 45.6% of the market in 2023. This dominance can be attributed to advanced diagnostic accuracy and efficient analysis of medical data. Adoption has been rising across hospitals and research institutions. These solutions support telemedicine, fraud detection, dosage optimization, robotic surgeries, and cybersecurity. Strategic partnerships, including GE Healthcare’s alliances in China to develop the Edison AI platform, have further strengthened the software segment’s position and accelerated digital healthcare transformation.

Technology segmentation in this market includes Machine Learning, Querying Method, Deep Learning, Context Aware Processing, and Natural Language Processing. Deep Learning held a leading share of 36.2% in 2023. Its growth has been supported by powerful data-processing abilities and automated medical tasks. Deep learning algorithms integrate varied medical datasets over time to improve treatment precision. Meanwhile, Natural Language Processing is projected to record a 37.4% CAGR, driven by faster clinical decision-making and improved physician efficiency through automated data interpretation.

In the therapeutic landscape, oncology represented the largest share at 47.6% in 2023. The segment benefited from AI’s strong role in early cancer diagnosis, treatment planning, and improved patient outcomes. Rising global cancer incidence and enhanced medical infrastructure have contributed to segment expansion. AI technologies are enabling accurate predictive models for cancer progression. According to global health estimates, cancer caused approximately 10.3 million deaths in 2020, highlighting the continued need for precision medicine solutions supported by artificial intelligence.

Neurology is anticipated to emerge as one of the fastest-growing therapeutic segments within AI in precision medicine. A CAGR of 34.8% is expected, supported by rising cases of neurological disorders, including epilepsy, dementia, migraines, and Alzheimer’s disease. Increasing disease awareness and expanding diagnostic capabilities are improving adoption rates in neurological care. AI tools are supporting early diagnosis, personalized treatment, and monitoring of neurological conditions. Advancements in healthcare technology and clinical data integration continue to stimulate demand in this segment.

Key Players Analysis

The competitive landscape for AI in precision medicine is shaped by firms employing innovation-driven strategies. Growth has been supported through product launches, strategic partnerships, and regulatory approvals. Investments in AI-driven diagnostics and treatment platforms have strengthened industry presence. Collaboration with healthcare systems and research institutes has enhanced patient-specific outcomes. Novo Nordisk, GE Healthcare, and Alphabet Inc. continue to allocate capital toward algorithm advancement and clinical integration. Sanofi and Tempus have also emphasized therapeutic personalization and data-driven clinical insights to broaden applications across disease areas.

Market expansion has been reinforced through sustained mergers, acquisitions, and research funding. Companies have prioritized scalable AI models, cloud platforms, and precision analytics to accelerate adoption in clinical workflows. Emphasis has been placed on expanding regulatory-approved solutions to secure commercial advantages. NVIDIA Corporation, Intel Corporation, and Microsoft Corporation are focusing on computing infrastructure and interoperable platforms. Their capabilities support faster model development, enabling broader deployment across pharmaceutical research and clinical settings.

Cost-effective offerings and real-time decision support technologies remain key drivers of competitive success. The launch of advanced AI drug discovery platforms has accelerated precision therapy design and genomic-based treatment optimization. AstraZeneca and Atomwise Inc. are investing in protein-target prediction and compound screening systems. Insilico Medicine and BioXcel Therapeutics, Inc. are concentrating on AI-enabled clinical pipelines. Such initiatives are expected to streamline drug development, reduce costs, and improve precision treatment accuracy across oncology, neurology, and rare disease therapeutics.

The expanding regulatory focus has encouraged companies to align product innovation with compliance frameworks. Regulatory approvals have increased market reach and strengthened stakeholder confidence. According to industry reports, personalized drug approvals in major markets illustrate rising acceptance. Tempus, Enlitic Inc., and Zephyr AI are advancing predictive analytics, imaging intelligence, and risk-assessment technologies. Modernizing Medicine Inc. is embedding AI in clinical records and decision tools. These actions reinforce leadership positions and support continued growth in precision-driven healthcare delivery.

Challenges

1) Data quality, bias, and representativeness

Genomic and biobank data still show uneven population coverage. Most datasets are dominated by European ancestry, often above 80% in many genome-wide studies. This imbalance can weaken model accuracy, especially for non-European patients. It also raises fairness issues when applying precision medicine across diverse groups. Institutions such as NIST have cautioned that AI systems can amplify harm if bias is not controlled. Continuous data review, improved representation, and bias checks across the model lifecycle are required. Strong governance frameworks and transparent dataset audits support reliable and equitable precision medicine outcomes.

2) Privacy, consent, and data sharing

Genetic and health information is treated as highly sensitive in major regulations. Under GDPR, it falls into a special category that requires explicit legal bases and protective controls. HIPAA also imposes strict rules on patient privacy, security safeguards, and de-identification. These requirements protect individuals but can slow large-scale model development. Cross-border research and multi-institutional studies face delays without early compliance planning. Secure federated learning and standardized consent frameworks can ease collaboration. Clear data-sharing agreements, robust cybersecurity, and documented governance help maintain trust and ensure ethical use of precision health data.

3) Interoperability and fragmented data

Electronic health record adoption has increased, yet seamless data exchange remains limited. Many hospitals cannot consistently access or use external medical records at the point of care. Gaps in standards, integration workflows, and data formats reduce the value of precision medicine systems. Incomplete or inconsistent data can weaken model insights and reduce clinical impact. National health IT programs report progress, but usage remains uneven across providers. Strong interoperability standards, better data pipelines, and real-time exchange systems are necessary. Unified health data infrastructure supports accurate AI-driven insights and improves clinical decision support.

4) Clinical validation and generalizability

AI systems in precision medicine must show reliable performance across real-world settings. Models trained in one environment may lose accuracy when used in another due to population, workflow, or technology differences. Prospective trials, multi-site evaluations, and long-term monitoring are essential. Regulators emphasize data quality, cybersecurity controls, and credible performance claims. Ongoing validation reduces the risk of performance drift after deployment. Continuous monitoring tools and post-market checks support safe use. Robust evidence and transparent reporting strengthen clinician confidence and help AI tools deliver consistent results across diverse patient groups and clinical contexts.

5) Regulatory complexity and change management

AI for precision medicine operates under evolving regulatory frameworks. The EU AI Act classifies medical AI as high risk and requires strict controls, such as risk management, human oversight, and high-quality data processes. In the United States, pathways like FDA’s Predetermined Change Control Plan demand clear documentation and structured change governance. These rules ensure safe model updates and transparency. Development teams must align design controls, cybersecurity plans, and post-market surveillance with regulatory expectations. Effective compliance planning and structured change management improve approval timelines and reduce adoption barriers in healthcare settings.

6) Explainability, transparency, and human factors

Trust remains a key barrier to medical AI adoption. Many advanced models work as complex “black boxes,” which makes it difficult for clinicians to understand decision processes. Regulators call for clear information, risk communication, and strong human-AI collaboration. Systems must provide insights that clinicians can verify and question. Without transparency, adoption slows and clinical confidence declines. Explainable outputs, user-friendly interfaces, and decision support design improve usability. Training and human-factor research help ensure safe operation. Balanced innovation and clarity help build trust while maintaining high-performance AI in precision medicine.

Opportunities

1) Earlier and more accurate diagnosis

AI adoption in diagnostic imaging has expanded. The technology is being used across radiology, cardiology, ophthalmology, and several other specialties. It supports faster and more accurate detection of disease. It also helps doctors manage large imaging volumes. Regulatory approvals in the United States show steady progress. A growing number of AI-enabled medical devices have been authorized. These tools support triage, detection, and quantification tasks in clinical workflows. As approved indications broaden, diagnostic pathways are becoming more efficient. It is expected that earlier disease identification will reduce treatment delays and improve care outcomes at scale.

2) Genomics-driven therapy selection

Sequencing costs have fallen quickly in recent years. This shift makes population-wide genomic testing more practical. AI tools now help review large genetic datasets. They identify priority variants and predict likely drug responses. They also support faster clinical trial matching. This enables treatment strategies that are tailored to an individual’s genetic profile. As a result, care pathways are becoming more precise and efficient. It is expected that patient outcomes will improve through targeted therapies. Broader access to genomic data and AI analysis will strengthen personalized medicine programs.

3) Smarter clinical trials and R&D

Clinical research teams are adopting AI to accelerate drug development. Recent FDA guidance for 2025 describes how AI may be used in regulatory evaluation. This includes models that assess safety, effectiveness, and product quality. Opportunities are emerging for synthetic control arms and predictive patient selection. Automated evidence synthesis is also expanding. These capabilities can shorten trial timelines and improve data reliability. As AI methods gain regulatory trust, research organizations will scale adoption. Efficiency gains are expected in design, recruitment, and data monitoring. Faster evidence generation will support quicker access to validated medical therapies.

4) Real-world evidence and continuous learning

The FDA’s PCCP framework enables AI systems to update after approval. Models can learn from real-world data within a controlled plan. This approach maintains patient safety while improving performance over time. Continuous learning systems are expected to reduce model drift and increase accuracy. Health systems will benefit from ongoing algorithm refinement without repeated full approvals. Real-world data integration also supports broader evidence development. This strengthens the link between daily clinical practice and regulatory standards. The result is a more adaptive and reliable AI ecosystem in healthcare.

5) Interoperability tailwinds

Healthcare organizations are expanding use of FHIR-based data exchange. Standard APIs enable secure access to patient records across systems. This reduces integration complexity for AI developers. It also ensures consistent data pipelines across hospitals and clinics. Standardization lowers deployment costs and accelerates adoption of clinical AI tools. Better data flow supports decision support, automation, and population-level analytics. As interoperability improves, precision medicine platforms gain stronger infrastructure. Faster information exchange is expected to advance patient care coordination and analytics-driven interventions.

6) Risk-managed adoption at scale

Clear regulatory guidance is guiding responsible AI deployment in healthcare. Frameworks from NIST, FDA, MHRA, and Health Canada highlight quality and safety expectations. They support governance, transparency, and risk management. These standards help organizations build trust and scale AI programs safely. Structured compliance frameworks reduce uncertainty for clinical and enterprise teams. Adoption can proceed faster when security and ethical measures are defined. As global standards align, healthcare systems will integrate AI more confidently. This balanced approach protects patients while accelerating innovation in precision medicine.

Conclusion

The AI in precision medicine market is poised for sustained growth as healthcare systems move toward more personalized and data-driven care. Advancements in electronic health records, genomics, and digital diagnostics are improving treatment decisions and patient outcomes. Supportive policies, regulatory clarity, and increasing global collaborations are strengthening confidence among investors and healthcare providers. Ethical practices, secure data use, and better interoperability remain essential to ensure responsible adoption. Continued improvements in model accuracy, clinical validation, and real-world evidence will further enhance trust and expand use. As technology matures, AI-powered precision medicine is expected to transform disease detection, therapy planning, and long-term patient management across diverse clinical environments.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)