Table of Contents

Overview

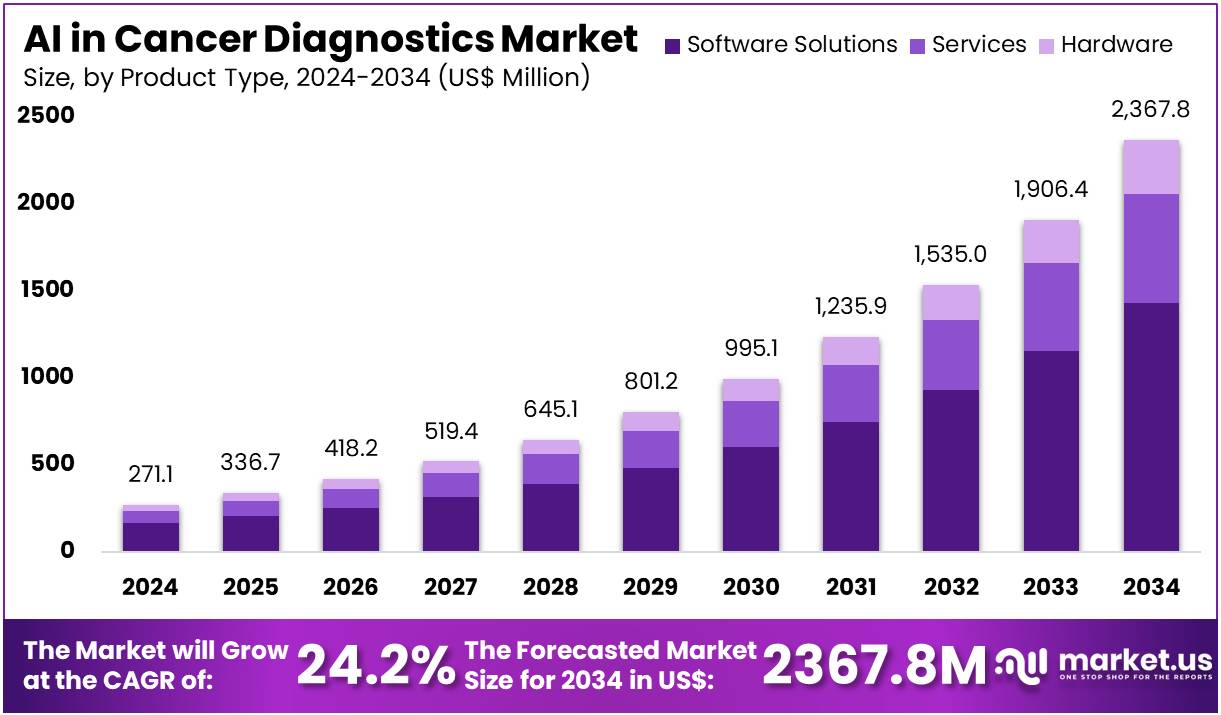

New York, NY – July 31, 2025 – The AI in Cancer Diagnostics Market size is expected to be worth around US$ 2,367.8 Million by 2034 from US$ 271.1 Million in 2024, growing at a CAGR of 24.2% during the forecast period 2025 to 2034.

In 2024, the global AI in cancer diagnostics market is witnessing significant momentum, driven by rising cancer prevalence, growing adoption of precision medicine, and increasing demand for early, accurate, and cost-effective diagnostics. Artificial intelligence (AI) is being integrated across diagnostic modalities such as imaging, pathology, genomics, and clinical decision support, enhancing detection speed and diagnostic accuracy.

The market is segmented by component (software, hardware, and services), application (breast cancer, lung cancer, colorectal cancer, prostate cancer, and others), and end-user (hospitals, diagnostic laboratories, research institutes, and oncology centers). Among these, software solutions dominate due to rapid advancements in AI algorithms, image recognition, and cloud-based analytics.

North America currently leads the market, supported by advanced healthcare infrastructure, robust research investments, and favorable regulatory initiatives for AI integration. Meanwhile, the Asia-Pacific region is projected to register the fastest CAGR, driven by rising cancer incidence, digital health expansion, and growing healthcare expenditure.

AI-powered cancer diagnostics have shown promising results in reducing false positives and negatives, supporting early-stage detection, and aiding personalized treatment plans. Studies by the National Cancer Institute and NIH indicate that AI tools can improve diagnostic accuracy by over 15% in some imaging applications. As AI technologies mature and regulatory pathways evolve, the market is expected to reach substantial value by 2034, reflecting a transformative shift in global cancer care.

Key Takeaways

- In 2024, the global market for AI in cancer diagnostics was valued at approximately US$ 271.1 million and is projected to reach US$ 2,367.8 million by 2034, expanding at a robust CAGR of 24.2% over the forecast period.

- By product type, the market is categorized into software solutions, services, and hardware. Among these, software solutions emerged as the leading segment in 2023, accounting for a 60.4% market share, driven by advancements in AI algorithms and integration with diagnostic imaging platforms.

- In terms of application, the market is segmented into breast cancer, brain tumors, colorectal cancer, lung cancer, and others. Breast cancer remained the dominant application area in 2023, representing 35.0% of the overall market, supported by the growing emphasis on early detection and high prevalence rates globally.

- Based on end-user, the market is divided into hospitals, surgical centers & medical institutes, and others. The hospital segment led the market, holding a 52.8% share due to increased deployment of AI-enabled diagnostic systems and higher patient footfall.

- Regionally, North America commanded the largest share of the market in 2023, accounting for 48.3%, attributed to advanced healthcare infrastructure, high AI adoption, and supportive regulatory frameworks.

Segmentation Analysis

- Product Type Analysis: Software solutions accounted for 60.4% of the AI in cancer diagnostics market, driven by the growing use of AI algorithms in medical imaging and data interpretation. These tools enhance diagnostic accuracy by analyzing complex datasets and identifying cancerous patterns more efficiently than traditional methods. The adoption of deep learning technologies, along with integration into EHRs and laboratory systems, is accelerating clinical decision-making and workflow optimization, particularly in high-volume healthcare settings such as hospitals and diagnostic labs.

- Application Analysis: Breast cancer represents the largest application segment, holding a 35.0% share of the AI in cancer diagnostics market. The high global prevalence of breast cancer and increasing emphasis on early detection are driving this trend. AI technologies are being widely implemented to analyze mammograms, MRIs, and ultrasound images, improving detection accuracy and reducing diagnostic delays. As global screening programs expand and personalized treatment becomes more common, demand for AI-powered breast cancer diagnostics is expected to rise steadily.

- End-User Analysis: Hospitals dominate the end-user segment with a 52.8% market share, reflecting their early adoption of AI in radiology and oncology departments. The rising complexity of cancer diagnostics and increasing patient volumes have led hospitals to implement AI tools for faster, more accurate analysis of biopsies, scans, and genomic data. These technologies support clinical decision-making, improve workflow efficiency, and enhance treatment outcomes. Additionally, hospitals are leveraging AI to advance cancer research and streamline operational management.

Market Segments

By Product Type

- Software Solutions

- Services

- Hardware

By Application

- Breast Cancer

- Brain Tumor

- Colorectal Cancer

- Lung Cancer

- Others

By End-user

- Hospital

- Surgical Centers & Medical Institutes

- Others

Regional Analysis

North America Leads the AI in Cancer Diagnostics Market

North America accounted for the largest revenue share of 48.3% in the global AI in cancer diagnostics market, driven by increasing investments in precision medicine, widespread adoption of digital imaging technologies, and a strong focus on early cancer detection. AI-based solutions are playing a transformative role in interpreting complex medical images such as CT scans, mammograms, and pathology slides—thereby enhancing the diagnostic accuracy of radiologists and pathologists.

A supportive regulatory environment further strengthens market growth. The U.S. Food and Drug Administration (FDA) has been actively approving AI-enabled medical devices for oncology. According to FDA records, 30 AI/ML-enabled devices were cleared in 2022, rising to 52 in 2023, and reaching 30 more by May 2024. These approvals span key diagnostic applications including breast and prostate cancer detection.

Major medical technology providers are investing heavily in AI integration. Siemens Healthineers reported a 5.6% revenue growth in its Diagnostics segment in FY 2024, attributing the increase in part to growing demand for AI-enhanced diagnostic systems across North America.

Asia Pacific to Witness the Fastest Growth Rate

The Asia Pacific region is projected to register the highest CAGR during the forecast period, supported by a growing cancer burden, expanding digital healthcare infrastructure, and heightened focus on early diagnosis. Rapid adoption of medical imaging systems across countries such as China, Japan, and India is generating large datasets essential for AI training and deployment.

China’s healthcare expenditure reached CNY 8.5 trillion (US\$1.2 trillion) in 2022, with a considerable portion directed toward advanced diagnostic technologies, as reported by the National Health Commission. Similarly, Japan’s Ministry of Health, Labour and Welfare has initiated strategies to incorporate AI into clinical workflows to address the challenges posed by an aging population and rising incidence of chronic illnesses, including cancer.

Global diagnostic companies are also driving regional expansion. For instance, Philips reported €7.1 billion (US\$7.6 billion) in sales from its Diagnosis & Treatment businesses in 2024, with strong contributions from Asia Pacific markets. This reflects increasing demand for AI-integrated cancer diagnostic tools across the region.

Emerging Trends

- Advancement of Biomarker-Driven Detection: The integration of AI with molecular biomarker analysis has been accelerated by programs such as the NCI’s Early Detection Research Network. AI algorithms are being applied to large biomarker datasets to identify subtle molecular changes indicative of early cancer stages, fostering non-invasive tests capable of detecting progression before symptoms appear.

- Growth of AI-Enabled Medical Devices: The FDA’s dedicated “AI-Enabled Medical Device List” has expanded significantly, reflecting a broadening portfolio of AI tools authorized for oncology applications, from digital pathology to radiomics platforms. This growth underscores increasing regulatory confidence in AI’s safety and effectiveness for clinical use.

- Establishment of Robust Regulatory Frameworks: In March 2024, the FDA published a coordinated policy outlining how its centers (CDER, CBER, CDRH, OCP) will collaborate to evaluate AI/ML medical products. This “Artificial Intelligence and Medical Products” guidance lays out principles for transparency, performance monitoring, and predetermined change control, setting clear expectations for developers and expediting innovation while maintaining patient safety.

- Integration of Multimodal Data Streams: AI models are increasingly trained on combined inputs imaging, genomics, and electronic health records to enhance diagnostic accuracy. By merging radiomic features with molecular profiles, these multimodal systems can distinguish cancer subtypes more precisely and predict progression risks in a single assessment, marking a shift toward holistic AI diagnostics.

- Emphasis on Explainability and Trust: With clinical adoption rising, there is a growing focus on “explainable AI” methods that allow clinicians to understand model decisions. Regulatory bodies and research consortia are prioritizing interpretability standards to ensure that AI outputs can be traced to underlying biological or imaging features, thereby promoting clinician trust and facilitating informed decision-making.

Use Cases

- Breast Cancer Screening (Digital Mammography): AI-powered tools such as ProFound AI® V4.0 have been cleared by the FDA to assist radiologists in detecting soft-tissue densities and microcalcifications on digital breast tomosynthesis exams. These systems operate in real time alongside the interpreting physician, improving lesion detection rates without adding significant workflow burden.

- Prostate Cancer Diagnosis (Histopathology): AI-augmented workflows are under evaluation in clinical studies to reduce reliance on additional stains. For example, trials registered on ClinicalTrials.gov (e.g., NCT07060599) are comparing AI-assisted H&E slide analysis against traditional immunohistochemistry, aiming to streamline diagnosis in routine core needle biopsy cases.

- Skin Cancer Detection (Teledermatoscopy): Teledermatology platforms are integrating AI algorithms to pre-screen dermatoscopic images for melanoma and non-melanoma skin cancers. Trials such as AIDMel (NCT06080711) are assessing the impact of AI on diagnostic accuracy and workflow efficiency in remote settings, where dermatology expertise may be limited.

- Multi-Cancer CT Screening: Non-contrast CT studies (e.g., NCT06632886) are exploring AI models capable of detecting lesions across lung, liver, gastric, and other tissues in a single scan. Early results suggest that automated lesion detection can flag suspicious regions for radiologist review, potentially reducing missed diagnoses and accelerating follow-up care.

- Colorectal Polyp Detection (Endoscopy): Software like SKOUT® has been FDA-cleared for use during white-light colonoscopy to highlight potential polyps in real time. By augmenting endoscopic video feeds, these AI tools support clinicians in identifying subtle mucosal changes, with ongoing studies evaluating impact on adenoma detection rates.

Conclusion

The global AI in cancer diagnostics market is undergoing rapid transformation, driven by rising cancer incidence, advancements in AI technology, and a growing emphasis on early and accurate detection. With strong adoption across imaging, pathology, and genomics, AI is improving diagnostic precision and clinical workflows.

North America leads in regulatory support and implementation, while Asia Pacific is poised for the highest growth. Emerging trends such as multimodal data integration and explainable AI are reshaping diagnostic standards. As clinical validation expands and regulatory frameworks evolve, AI is expected to play a central role in the future of global cancer diagnostics.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)